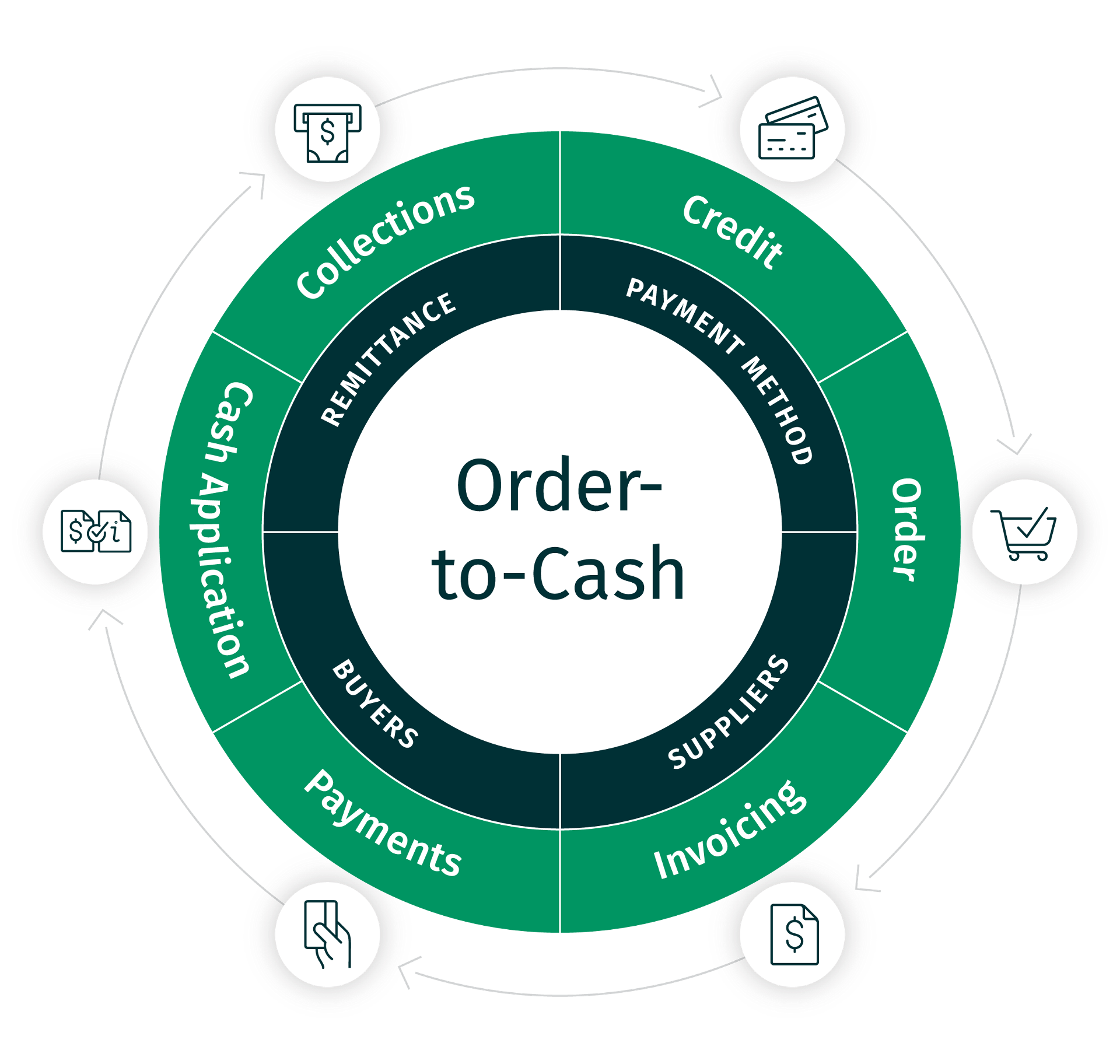

The Order-to-Cash Cycle

Often abbreviated as as O2C, the Order-to-Cash cycle is the complete process your business undertakes to accept an order, extend credit, deliver the goods or service, collect payments and report on the process.

The strategic value of optimizing the Order-to-Cash cycle

Companies of all sizes benefit from analyzing and improving their Order-to-Cash cycle because the O2C impacts so many aspects of their business:

- Customer relationships

- Cash flow

- Order fulfillment timescales

- Credit replenishment / sales potential

- Working capital costs

- Insight into business health

The Order-to-Cash cycle: step by step

Step 1: Credit Approval

Credit approval is the first step in the order-to-cash (O2C) cycle. In B2B transactions, companies purchase goods and services on credit. Credit approval involves the supplier approving credit requests and credit limits for their customer.

To determine how much credit to grant a customer, a credit management professional will pull credit reports on the customer from the credit bureaus, consult the customer’s bank and ask other businesses about their experiences with the customer (these are referred to as trade reports).

Another important part of the credit approval step is analysing the supplier’s own financial situation. After analyzing the supplier’s cash-on-hand, cash flow and outstanding receivables, the credit professional will be able to place a responsible limit on customer credit.

Credit approval professionals will work hand in hand with sales to set the payment terms of the customer’s potential order. Payment terms include when payment is due, any discounts available for paying early as well as any penalties that will be incurred if payment is late.

The credit management professional is responsible for enabling maximum sales volumes at their company while minimizing risk. It is a difficult and high-stakes discipline. Consequences for extending credit to customers who can’t or won’t pay on time include cash flow problems, increased DSO and even losses.

Step 2: Order acceptance

Sales teams work with customers to place an order. Sales professionals inform the customer about what goods and services are available and negotiate with them on aspects of the order like price, quality thresholds, delivery dates and payment terms.

Step 3: Order fulfillment

If fulfilling a good, order fulfillment involves locating the items, preparing them and shipping while ensuring that all delivery details are correct. When fulfilling a service, order fulfillment involves arranging the date and location of service and following through on all services promised in the order.

Step 4: Customer invoicing

The delivery of a good or service requires accounts receivable professionals to now invoice the customer for the amount owed. This happens in a variety of ways, either via a paper bill sent through the mail, or increasingly, through ePresentment or electronic billing. Electronic invoices include older formats such as faxes and phone (interactive voice response). Newer, more efficient formats include emailed bills and bills presented via portals.

Quickly and accurately generating invoices and delivering them to customers is important and time-sensitive work. The faster the invoice presentment to a customer, the faster they can pay and realize cash for the business. either via a paper bill sent through the mail, or increasingly, through ePresentment or electronic billing.

Step 5: Payment process

Customers will try to pay their suppliers in the ways that are most convenient and beneficial to them. This may include paper checks, ACH payments, wire-transfers or virtual credit cards.

The supplier must decide which form of payments they are willing to accept and set up processes to maximize the efficiency of receiving payments through their chosen channels.

There are costs and efforts associated with receiving each type of payment, and businesses must balance honoring customer payment preferences with their own interests.

Step 6: Cash application

Once payments have been received via the various payment channels, cash must be "applied" to accounts. In practice, this means recognizing that a certain amount of cash has been received and marking an invoice as paid.

This is more complex than it seems. Companies typically receive hundreds or thousands of payments each month. Cash application specialists must then "match" cash received with invoices. The use of remittance advice (often referred to simply as "remittance") assists with this. Some forms of payment, like paper checks and credit card payments come with remittance advice attached. A check may have in its "memo" section a note that states it is paying off invoice #1358. But some forms of remittance, such as ACH do not support remittance advice coming attached with the payment. There many ways to send remittance advice. For instance, in an email or phone call. This complicates the work of applying the cash and requiring advanced cash application solutions to ensure speed and accuracy.

Further complications arrive when payments are meant to cover multiple invoices, when customers short pay for various reasons or when payment errors occur.

The faster that received cash is applied, the faster a business can reliably use it for operations and the faster a customer's credit can be replenished, enabling them to order more goods.

Step 7: Collections

When payment is not received and applied by the agreed upon date, an account becomes delinquent and is to transferred to collections.

It is the job of collectors to contact customers and try to get them to pay. There are many reasons that accounts become delinquent. A customer could just need a reminder to pay their open invoices, they may be strategically paying late in order to better manage their own cash flow, they may have a dispute about the good or service they received or they may simply be unable to pay.

A collector has the complicated job of connecting with customers, understanding their reasons for delinquency and trying to work with them in order to realize payment for the company.

Now that you have an understanding of the essential processes of the Order-to-Cash cycle, let’s look at ways you can optimize the order-to-cash (O2C) in your business.

Order-to-Cash best practices

Often overlooked and under-leveraged as an opportunity, the order-to-cash process can drive business efficiency, increase cash flow and strengthen customer relationships.

Companies that approach this process with strategic goals in mind gain considerable advantage over those that do not. While it’s important for a business to recognize the opportunity to reduce costs involved in the order-to-cash process, the benefits of investing in smart Order-to-Cash solutions go much further.

Invoicing and payment acceptance best practices a logical starting point

Topping the list of value-creating order-to-cash (O2C) strategies are intelligent invoice design and Electronic Invoice Presentment and Payment (EIPP). For customers to pay on time, they must understand electronic invoices. Using an integrated payment acceptance solutions can help speed up the customer invoicing and payment process.

Optimizing paper invoice and statement delivery is no longer enough. Modern invoicing systems require multiple options for delivering invoices, as well as for payment. Electronic invoicing virtually eliminates invoice delivery time to customers, helping cash get in the door faster.

Automated, intelligent cash application: advanced solutions

The order-to-cash (O2C) cycle begins with invoice delivery and payment but isn’t complete until cash is properly applied.

Once payment is received, the funds have to be accurately applied (posted to a system of record) for a company to realize payments as revenue. Delays in cash application put DSO at risk.

Cash application is challenging because buyers pay in a variety of ways. For instance, by check to a lockbox, directly to headquarters or at a remote location. The data on checks must be captured, which often involves manual keying. Even when buyers submit electronic payments, they frequently come decoupled from the invoice, making matching a resource-intensive task. Exception handling poses yet another challenge. As much as a business strives for 100 percent match rates, the reality is that exceptions will occur. Handling exceptions takes time and resources and is a big cause of increasing DSO.

Automating the cash application process end-to-end cuts costs and reduces DSO. Through technology, sellers can automatically extract transactional data from any source and intelligently match to open receivables, which can dramatically improve hit rates whether payments are by check or electronic. Having a user-friendly tool to efficiently work through the inevitable exceptions can get payments posted quicker without dependence on a large manual staff.

Increased brand loyalty through better customer experiences

An order-to-cash (O2C) system should provide the same web-based archival and retrieval to both customers and call center personnel to securely research, view and print any invoice or statement.

The best order-to-cash systems also let customers manage and research their own invoices with easy-to-use web-based tools.

Conclusion

Order-to-cash (O2C) has the potential to be a strategic linchpin of your business. If done right, it represents an opportunity for improved cash flow, increased customer satisfaction, movement toward corporate sustainability and, of course, measurable cost reduction.

When evaluating solutions, ensure that they will be flexible enough to accommodate your customers’ needs for receiving invoices and making payments, that they address the critical last step of intelligent cash application and that there is a program in place to drive electronic adoption. With these three key capabilities, suppliers can get on track to achieving a perfect balance between buyer satisfaction and reduced days sales outstanding (DSO).