What are virtual credit cards?

Virtual credit cards are an electronic payment method that allows B2B buyers to securely pay their card-accepting suppliers by randomly generating a unique 16-digit card number, expiration date and security code. Virtual cards can be automatically generated to pay specific invoice(s), or can be issued for ad hoc purchases. There is generally no limit to how many virtual cards can be generated, however, many organizations have an established credit line for their virtual card program that cannot be exceeded by active card numbers.

Virtual credit card numbers exist to provide upfront control and back-end reconciliation. Because they are authorized to pay a specific supplier, for a set amount and for a defined duration, the risk of fraud is extremely low. Additionally, because they are tokenized, even if the card information is compromised by a fraudster (may create a data breach), the exposure is limited only to the amount of that virtual card account number.

Virtual cards can be configured with many different controls, including limiting the number of times they can be authorized or “swiped”, the time period for which they are valid, the types of businesses where they can be used, and of course the amount. Organizations can even specify an over/under tolerance in the event that the payment owed is different than the invoice.

In B2B purchasing, most businesses integrate their virtual card program directly into their ERPs and automatically issue them as part of their daily vendor payout for approved invoices, along with ACH and check payments.

Why do people use virtual credit cards?

Virtual credit cards are one of the most secure methods of electronic payment for online purchases. Upon taking a payment, many suppliers will keep their buyer’s payment information on file. They do this so that data does not need to be re-entered for every transaction. But if hackers gain access to that data they can use it to commit fraud.

A virtual card can be considered a token. This token protects the primary account number from being exposed. Token information is not useful to hackers. When generated, virtual cards have many controls and limitations. Fraudsters will find it extremely challenging to use a virtual card for an unauthorized purchase. In most cases, they would need access to the exact amount for which it's authorized. They also need to know the validity period and would need a special credit card processing terminal that can handle card-not-present transactions.

What benefits do virtual cards provide to buyers besides security?

Buyers get the added benefit of rebates from their virtual credit cards and float which is a period during which their suppliers are paid, but the buyers do not yet need to provide funds to their card issuer for the payment.

Suppliers pay a transaction fee for accepting a credit card payment. Credit card issuers make revenue from that fee and they share a portion of those funds with their customers, the buyer, in the form of a rebate. This incentivizes buyers to move their spending to credit cards to maximize that rebate.

These fees cut into the margins of suppliers and, as a result, suppliers sometimes will not accept credit card payments for certain transactions. The growing popularity of virtual credit cards with buyers has forced suppliers to develop payment acceptance strategies that will help them pay lower fees to accept business debit or credit cards.

Virtual credit cards play a part in an accounts payable automation strategy. They enable the automation of payments, reducing the steps required to pay invoices while retaining upfront controls.

What payment acceptance challenges do debit and credit cards pose for suppliers?

The main challenges for suppliers around virtual cards are fees and reconciliation difficulties.

Even though virtual credit cards automate the work of accounts payable, paradoxically they make the work of accounts receivable much more difficult unless a supplier is strategically managing their virtual card acceptance policies.

The main delivery method for virtual cards is through secure emails. To get paid, suppliers must identify and intercept those emails in high volumes. They manually key the credit card information and associated remittance into their systems unless the supplier has implemented an automated solution.

Suppliers who have high volumes of virtual card usage could potentially be interacting with multiple issuers and payment delivery methods on a daily basis.

When suppliers have a problem with a buyer's virtual card payment, they need to interact with the buyer's bank, adding another layer of complexity to resolving payment issues.

What are the fees associated with cards?

In every credit card transaction, there are three parties that may charge suppliers a fee.

The credit card issuer: This is the financial institution that issues the card. The issuer is generally a bank like Chase or Bank of America.

The credit card network: These are the companies that facilitate the transaction between the issuer and the merchant. The major credit card networks are Visa, Mastercard, Discover and American Express.

The payment processor: This is the company responsible for securing and carrying out the transaction. There are many third-party processors for suppliers to choose from.

What is an interchange rate?

Interchange represents the fees paid to or collected from the card-issuing banks that provide Visa, MasterCard, Discover and American Express cards.

Interchange creates incentives for payment network participants to maintain a reliable, dynamic and secure electronic commerce environment.

Suppliers can improve their processes and help qualify every card transaction for the most advantageous interchange fee.

What influences the interchange rate on virtual credit cards?

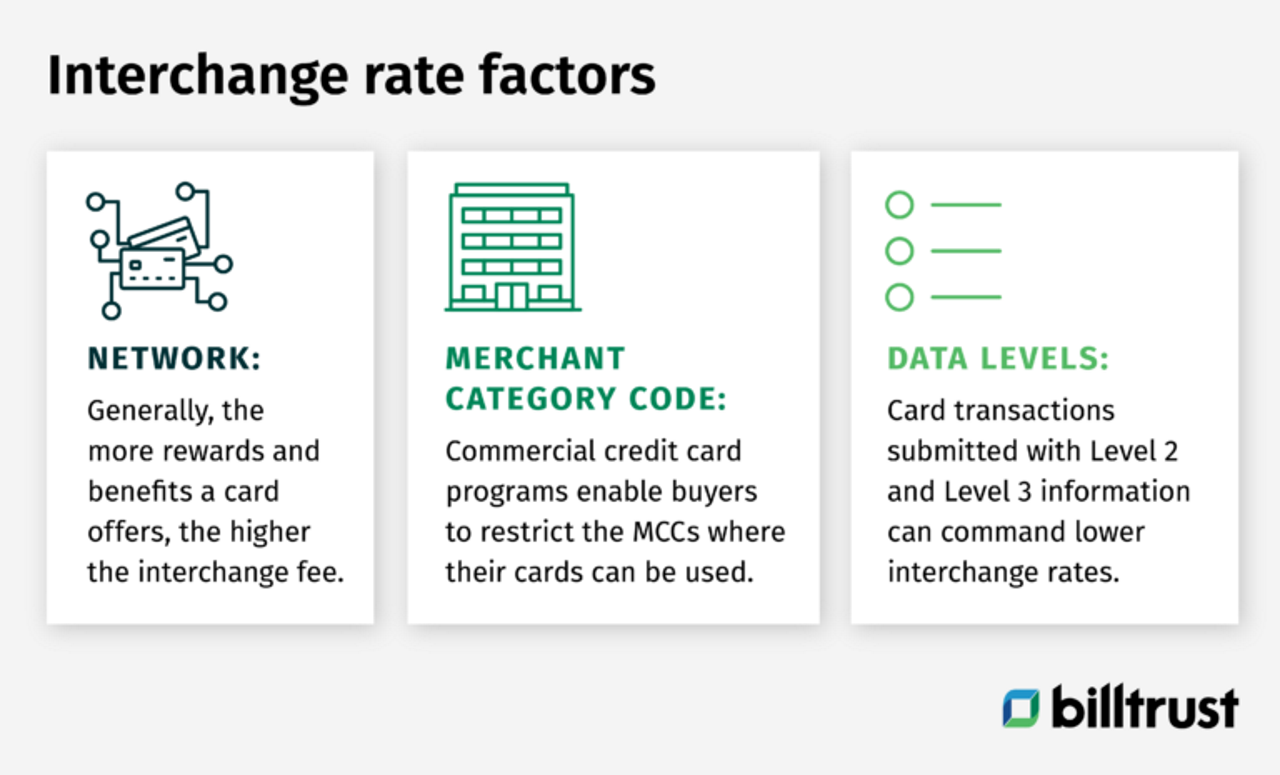

Because of the risk involved, credit card companies set and adjust their interchange rates regularly. In fact, interchange rates are based on a number of factors:

Network

Each of the four major credit card networks maintains their own table of interchange rates that vary depending on the type of card (e.g. consumer travel rewards card, commercial purchasing card). Generally, the more rewards and benefits a card offers, the higher the interchange fee.

Merchant Category Code (MCC)

MCCs are four digit numbers that indicate the category of the supplier’s business. Commercial credit card programs enable buyers to restrict the MCCs where their cards can be used (including virtual cards)

Data levels

Credit card processing has three categorization levels of data: 1, 2 and 3. Each level describes a certain amount of information about the payment. Level 1 includes the least information and Level 3 the most.

Card transactions submitted with Level 2 and Level 3 information can command lower interchange rates because credit card issuers have more confidence in the transaction being legitimate. But it can be challenging to submit Level 2 and Level 3 data with each transaction. In order to achieve this, suppliers will work with their merchant acquirer.

How to lower the costs of Virtual Credit Cards?

A supplier can lower their cost to accept virtual credit cards by pursuing lower interchange rates and processing fees, along with lowering their cash application costs.

Suppliers can lower their interchange rates by submitting Level 2 and Level 3 data with their transactions. Many suppliers look to outside vendors to help them achieve Level 2 and Level 3 data.

Suppliers can lower their processing fees (the additional fees paid to their payment processor) by negotiating their pricing structure or by using a membership-based model, wherein the supplier pays a monthly or annual membership fee to forgo additional fees beyond the interchange rate.

And finally, suppliers can lower the costs associated with applying the funds received from virtual credit cards by automating their payment acceptance and cash application processes. Even though virtual credit card payments come with remittance advice attached, most ERP systems cannot automatically apply the cash to open invoices. An automation vendor can help suppliers achieve straight-thru-processing of virtual credit card payments and save resources that would otherwise be diverted to the manual task of matching VCC payments to open invoices.

To learn how accounts receivable automation from Billtrust can help you accept virtual credit cards while lowering your costs to accept payments, fill out the contact us form and someone will be in touch!