What if your account receivable collections strategy could be powered by insights from 13 million buyers and $1 trillion annual transactions?

Billtrust sits on a mountain range of debtor data, and it’s telling a valuable story that every finance organization should use to optimize their collections activities. Through an intensive AI analysis, Billtrust has identified which payment reminders trigger the fastest invoice remittances, which communication channels are best for collections outreach, and which timeframes are the most effective for getting a response from delinquent buyers.

Ready to ditch your static dunning schedule and use the latest data intelligence for collections operations? Keep reading to understand why a one-size-fits-all approach is no longer effective and walk away with a new standard of AI-driven methods for reducing bad debt and improving corporate financial health with fewer write-offs.

Traditional Dunning Schedules Don't Work

Legacy AR collections procedures typically rely on rigid payment reminder schedules. Outreach is set on fixed intervals, and calls are made based on arbitrary dates. While these static approaches have long been considered “industry-standard practices,” they often lead to unintended consequences.

The Problem with Traditional Approaches

- Buyers are contacted too early or too often, blanketing them in frustrating communications that and deteriorate the customer experience

- One-size-fits-all approaches mean high-risk accounts get the same treatment as reliable ones

- Manual collections processes obscure success measurement and attribution — which nudge actually spurred the payment?

Macro-level trends can compound the issue, making ineffective collections practices increasingly risky.

These realities emphasize the deeper issue: AR leaders lack the data science resources to intelligently engage with customers about their overdue invoices.

That’s why Billtrust is empowering finance leaders to transform collections practices using AI. By applying advanced algorithms to Billtrust’s vast network of debtor behavior data, our experts have uncovered the next generation of best practices for collector teams. And we’re not just sharing these insights for the benefit of all; we’re putting these same AI tools to work in our clients’ own AR environments for even higher recovery rates.

Here are our research findings.

Research Reveals the Behavioral Science behind Smarter Payment Reminders

The first challenge in evaluating debtor behavior is pinpointing which action drove payment response. Was it the first touch, the last touch, or something in between? Thus, attribution becomes the lynchpin of success measurement. Attribution determines how you’ll assign credit for the payment action, and it’s a critical element of behavioral analytics. Common attribution models include:

First-touch attribution

Credit goes to the first reminder

Last-touch attribution

Credit goes to the last reminder before payment

Multi-touch attribution

Credit goes to multiple reminders

Linear attribution

Equal credit to all reminders

Time-decay attribution

More credit to reminders closer to the payment date

Billtrust’s research demonstrates that finance leaders should use a multi-touch attribution model but limit last-touch attribution credit to a 5-day window. Each collections outreach activity should have no more than five days to be deemed the touchpoint that spurred the buyer to pay. Five days offers the optimal balance between immediacy and typical lags in payment processing due to slower payment methods, weekends, or holidays.

At this point, many finance leaders can connect payment reminders to responses, but it’s not always clear how much debtor behavior must be observed before causation can be declared with confidence. When faced with this challenge, use this rule of thumb: At least 20% of your debtor population must exhibit activity before an action can be statistically reliable.

Attribution Best Practices:

Measure last-touch attribution using a 5-day window. Effectiveness increases significantly within 3-5 days. Anything shorter undercounts impact; anything longer clouds causation.

25% DSO Improvement

AR organizations can reduce DSO by up to 25% by adopting best-in-class collections practices, particularly through early intervention and higher automation.

Data Shows When and How Debtors Should Be Engaged

Reminders: Start 30 Days Out

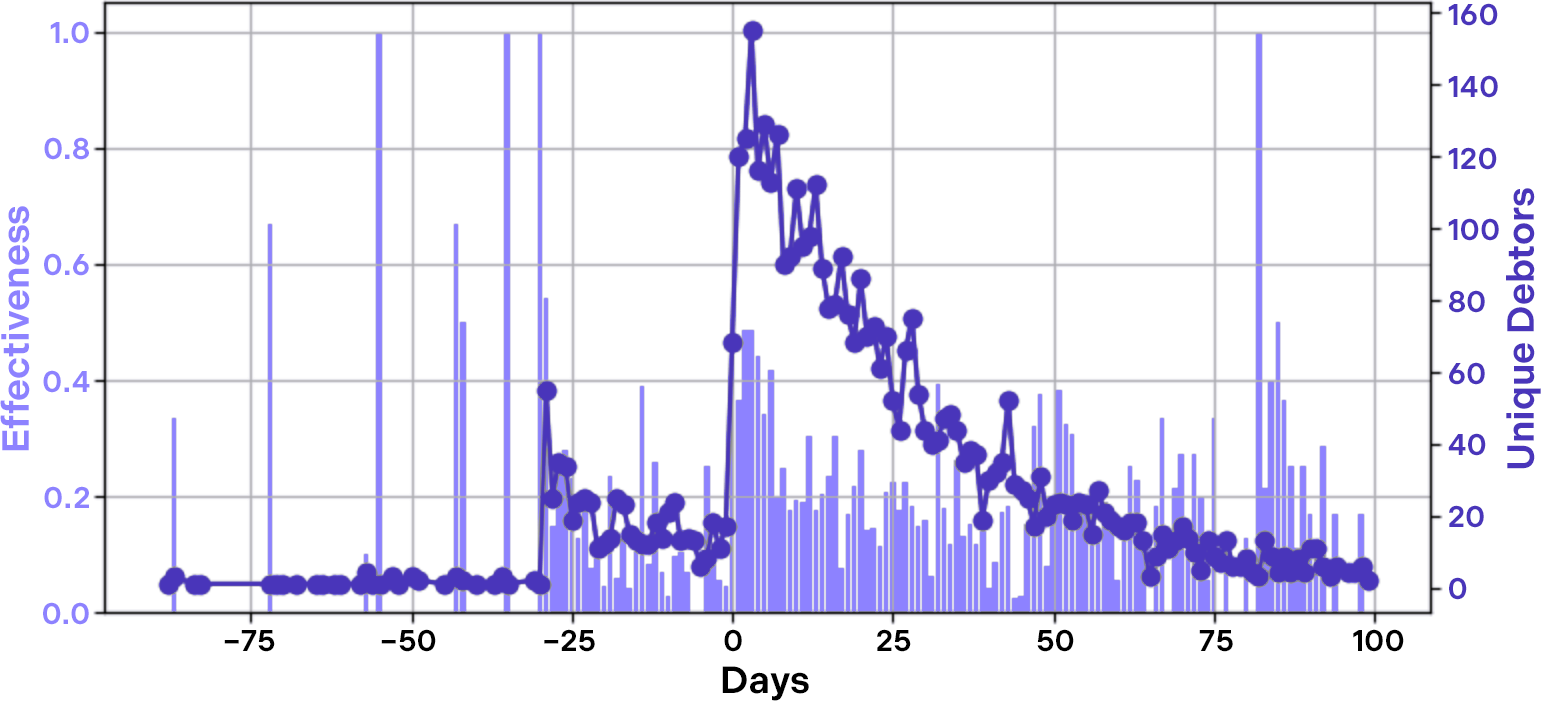

Data reveals that reminders (email and/or text) are most effective when sent starting 30 days before the due date, aligning with peak buyer responsiveness. Earlier outreach sees diminished returns.

Calls: If Payments are Due, it’s Time to Talk

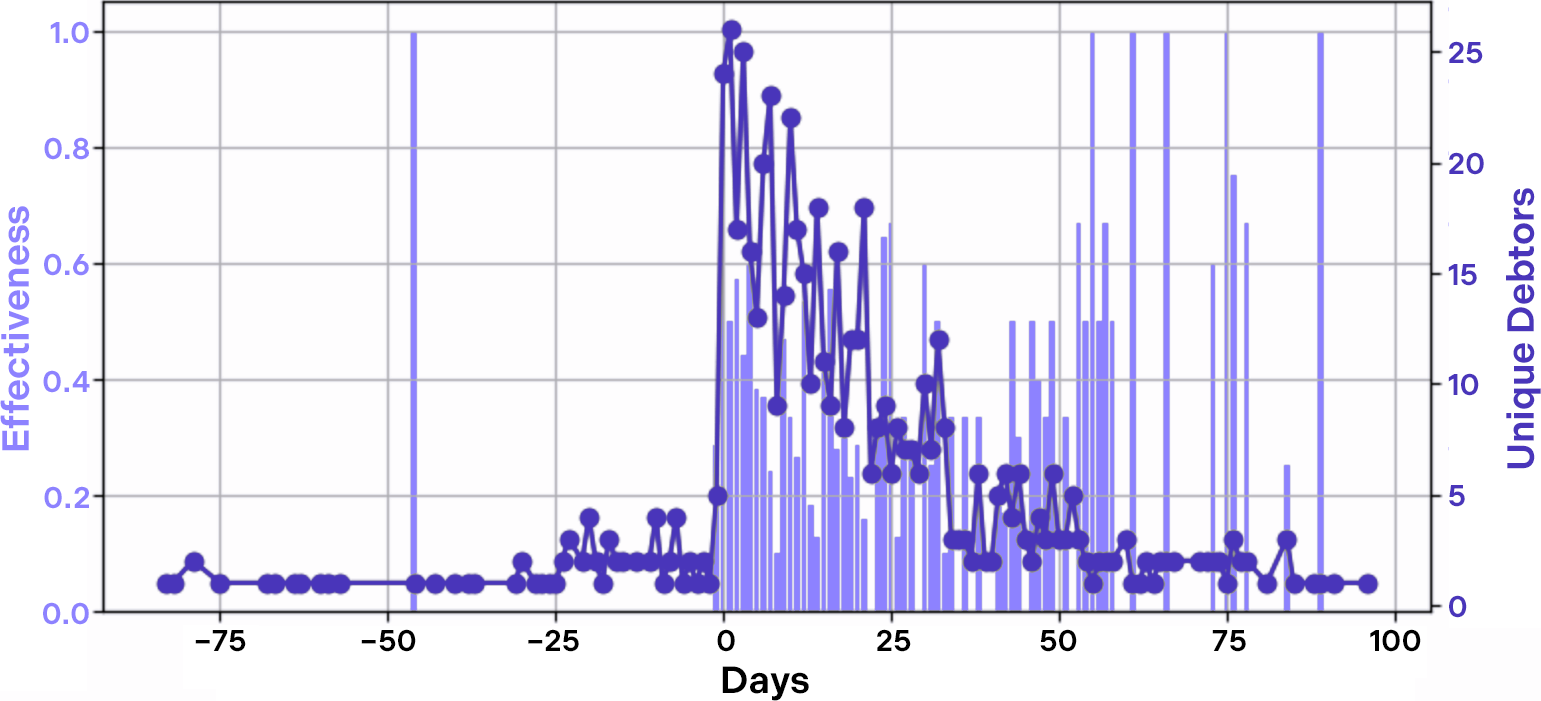

Calls are most impactful when placed the day before or on the due date. Earlier calls tend to be ignored or forgotten, likely because urgency hasn’t yet peaked.

Outreach Timeframes: 3 Best Practices

Email & Text Reminders:

–29 to +43 days from due date

Call Reminders:

–1 to +50 days from due date

Spacing: At least

5 days between touchpoints

Debtor Response to Reminders by Timing Relative to Invoice Due Date

Debtor Response to Calls by Timing Relative to Invoice Due Date

Segmentation: Using Debtor Data to Create Risk Groups

In accounts receivable, one size rarely fits all. Delinquent buyers differ not just in how much they owe, but in how they behave: how consistently they pay, how often they delay, and how they respond to outreach.

Billtrust’s research shows treating all accounts the same can reduce recovery rates. This is why segmentation is used to divide buyers into groups, so payment reminders can be tailored for higher response rates. Segmentation also helps collectors prioritize their efforts where it will have the greatest financial impact.

But to segment buyers, you have to have the right data.

Segmentation Alone Boosts Performance 15%

Customer segmentation is among the seven distinct management procedures that directly contribute to superior collections performance.

The Financial Data You’ll Need

Billtrust’s research shows these two metrics offer powerful guidance for segmentation:

- Monthly payment volume: Indicates financial capacity and transaction frequency

- Days delinquent per month: Aged (unpaid) balances reveal payment reliability and risk level

The Right Pressure at the Right Time:

“Segmentation is only as good as the data behind it. By analyzing patterns in payment timing, dispute frequency, and outreach response, we can group accounts not by guesswork, but by repeated behavior. This AI-driven approach allows AR teams to apply the right pressure at the right time.”

— Dave Ruda, Vice President of Product, Billtrust

Building the Risk Groups and Aligning Communications

Using these metrics, buyers can then be grouped into three risk segments:

- High Risk: High volume, high delinquency — these accounts require assertive, timely outreach, typically high-touch through multiple channels

- Mid Risk: Moderate volume and delinquency — benefit from balanced approach to engagement

- Low Risk: Low volume, low delinquency — respond well to gentle, low-touch reminders

In taking this segmentation model a step further, additional metrics can be taken into consideration, such as historical payment behavior, dispute frequency, and credit scores. Using multiple factors enables a more refined strategy for collections management, helping distinguish accounts that have a natural tendency to result in bad debt. To achieve this level of maturity, however, integration and unified management are required. Collections teams will need visibility into broader order-to-cash processes, such as invoice disputes, payment management, and credit management.

Based on these three groups, finance organizations can now build a more effective collections workflow aligning customized communications for each financial risk category.

AI-Powered Collections: 4 Procedures Spur Smarter Collections

The key to all of this? Avoid manual data analysis and labor-intensive outreach procedures. Best-in-class AR organizations leverage AI to automate these four critical steps:

Why Trust our Data? 13 Million Buyers Don’t Lie

Billtrust maintains the AR industry’s largest network of buyers and synthetic payment data for tracking and evaluating payment trends.

Real-time payment data from 13 million buyers across 1 million companies enables targeted recommendations for collections optimization. Plus, Billtrust handles $1 trillion in payments annually, meaning our source data has the volume needed to be statistically relevant. When data inputs are too small, inaccurate, or incomplete, even advanced analytical algorithms can come to the wrong conclusions. Billtrust, on the other hand, can facilitate intelligent recommendations.

We don’t just manage data, we engineer it. Billtrust carefully curates, cleans, and secures debtor behavior data, ensuring that our AI models use information that is anonymous, accurate, timely, and transparent.

Billtrust blends more than two decades of experience with data science, pressure testing AI-driven findings against 24 years of collections expertise to ensure recommendations make sense in the context of our deep industry experience.

Intelligent Segmentation with Billtrust

Billtrust offers an AI-powered segmentation engine that uses debtor behavior data to optimize collection outreach. As a capability within our Collections solution, it starts by intelligently segmenting your portfolio based on risk levels, then recommends the most effective outreach timing, methods, and cadence for each group. Billtrust leverages historic behavioral data to match customer accounts to the three risk segments (high, mid, low) as outlined in the section above. Customers receive a tailored collections schedule for each segment including a mix of communications with each action based on what’s worked well in the past. Procedures are built around attribution window best practices and other data-backed methodologies, driving superior results.

Here’s an example:

| Segment | High Risk | Mid Risk | Low Risk |

|---|---|---|---|

| Avg. Days Delinquent | 45+ | 30–45 | <30 |

| Recommended Start | -1 to +50 days | -15 to +30 days | -29 to +15 days |

| Action Mix | High frequency, multi-channel outreach | Balanced mix | Low touch, light reminders |

A Holistic Solution

Finance leaders who demand end-to-end visibility and efficiency enjoy Billtrust’s seamless integrations with more than 40 ERPs, banks, and financial institutions. They also appreciate the centralized management capabilities allowing transparency across collections, invoicing, payment, and credit activities. Clients can start with the Collections solution and expand when ready, reshaping AR operations from a series of disconnected workflows into a coordinated system for financial transparency.

Key Benefits of Billtrust Collections

Transform collections by turning behavioral data insights into actionable strategies.

- Autonomously segment your client portfolio by risk level, driving a targeted collections strategy

- Boost recovery rates by tailoring outreach communications for various types of debtors at scale

- Reach all segments – less delinquent accounts typically go under-served, but AI helps you gain full visibility and design smart outreach for all debtor groups

- Reduce manual effort, helping collectors automate and prioritize their efforts

- Improve customer retention through superior buyer experiences

Situations Evolve. The Solution Keeps Giving.

“Our AI engine continuously learns from buyer payment behavior, refining segments and updating outreach strategies over time. The result is a learning, living framework that evolves with your debtor portfolio. It’s the solution that keeps on giving.”

– Dave Ruda, Vice President of Product, Billtrust

Average Client ROI: 384%

How much ROI could you see from a Billtrust solution? Independent analyst firm IDC conducted in-depth research and finds that, on average, Billtrust solutions deliver 384% ROI. See how much time and money you could save with this report.

Demolishing $300K in Bad Debt

“In 2022 and 2023, we wrote up about $500,000 each year in bad debt. Now, we have less than $200,000 in our plus 90-day account. Billtrust helps us be more proactive in sending invoices and reminders to customers.”

— Ryan Oaks, Finance Director, Peak Industrial

Ready to Transform Your Collections Strategy?

Billtrust helps finance organizations turn debtor insight into impact. Get a personalized collections strategy consultation.