This post was originally published in June 2014 and was updated in Dec 2024 with more information about short payments, their effects on your business, and what you can do about them.

What is a short paid invoice?

A short paid invoice, also known as a short pay or short payment, occurs when customers underpay the amount due. This can happen for a variety of reasons, all of which hinder your company’s cash flow. Whether the reasons are expected (such as a known manufacturing delay) or unexpected (due to a customer cash flow problem), these short payments can cause your accounts receivable department to get stuck in the weeds while they identify, track down and resolve these inconsistencies. And while, yes, overpaying an invoice can also throw off balances, it occurs much less frequently than you might expect.

Understanding why your customers aren’t paying their invoices correctly and knowing how to deal with this when it does occur will help you avoid this wrench thrown into your accounts receivable (AR) process.

Read the blog → What is a short pay? How To handle short payments

Understanding the root causes of short payments

Why would customers short pay your invoices? Short pays can happen for a variety of reasons that can be categorized into three main groups:

- The customer disputes some of the charges on the invoice. This may be because the customer believes that the goods or services were not delivered as agreed. The goods were damaged during transport, or not all goods and services were delivered on time as agreed.

Another dispute relates to errors in the invoice. Maybe the customer had a valid reason for a discount or credit, and these trade promotions and marketing discounts were not reflected in the invoice. Earned discounts for early payment, or a payment plan that the collections teams had negotiated, were missing.

Sales tax can often lead to disputes. While your invoicing software may automatically charge sales tax for customers, some organizations may have a tax-exempt status. If you end up with a short-paid invoice, it’s likely a mistake on your part. Depending on your accounting software, you might have the option to include a non-profit designation or a tax-exempt deduction code, which can simplify the process of closing invoices. If not, you’ll have to handle these short pays manually.

- The customer is experiencing financial difficulties and is unable to pay the full amount immediately.

This may be temporary or it may be a sign of a more serious problem. Sometimes your customer can’t pay your invoice in full because they don’t have the cash on hand. Instead of working out a payment plan with you, they simply submit partial payments in order to keep you confused and working overtime. - The customer is trying to avoid paying the full amount.

In rare cases, customers may intentionally short pay invoices. This may be because they are trying to negotiate a lower price. Other companies have an unofficial policy to short pay every single invoice in order to manage cash flow. These organizations hope that suppliers like you can’t track their short pay properly, and will just write off the shortfall as a loss. These strategies may be unethical, and it’s up to your organization to develop policies and contract terms to protect against them.

Every now and then a short paid invoice is simply an innocent mistake. It happens, especially when manual invoicing and payment processes are being used. These errors rarely occur accidentally when electronic invoicing and payments are used with an EIPP portal.

Valid and invalid reasons for short paid invoices

At times, clients may make short payments intentionally as a way of protesting against an item, service, or combination of both. Other times, it’s an accident, where the person paying didn’t see the whole invoice.

A valid short pay is for a legitimate reason, and includes instances where businesses provide faulty goods or services, delivery of incorrect orders, over-pricing, or disputes between buyers and sellers.

An invalid short pay is one in which the buyer is breaking the contract and includes situations where buyers simply refuse to pay or withhold payment to negotiate a better deal. It’s crucial to ensure that contracts, terms, and agreements are clearly spelled out to avoid misunderstandings and conflicts.

Some of these invalid reasons may include:

- Human error.

- Unearned discount – taking advantage of an early pay discount after the deadline.

- Buyer only pays some invoices, not all, and doesn’t provide complete remittance information, complicating the cash application process.

- Buyer stretching the truth about delivery mistakes.

- Buyer changing their mind after the order was placed and in transit.

- Payment tactic to manage cash flow.

- Business strategy with the hopes that the supplier will write off the short pay.

The burden lies with you, the supplier, to research the issue, determine if it’s a valid dispute which needs to be rectified, or an invalid dispute, which needs to be resolved through collections.

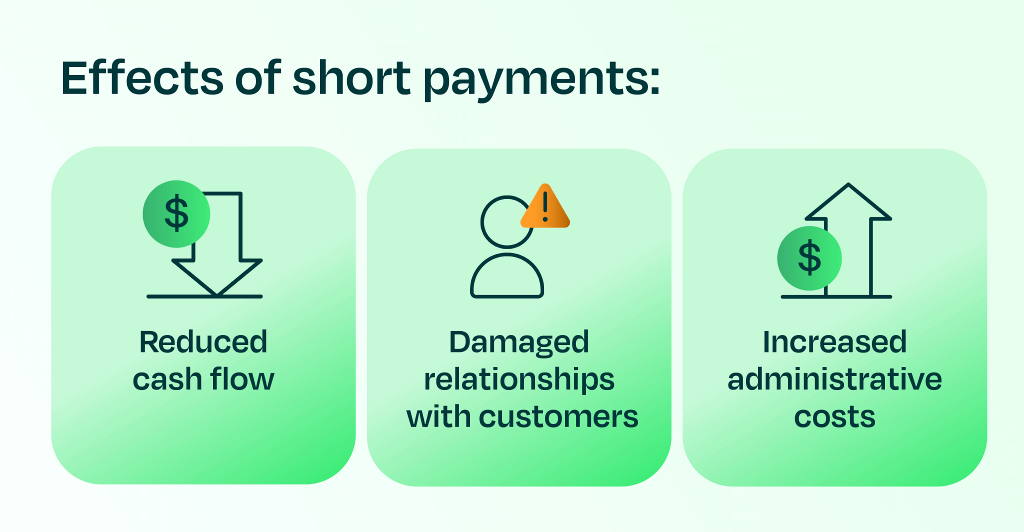

Impact of short payments on business

Regardless of the reason, short payments can be a major problem for businesses. Any credit, finance, or collections manager will tell you that short pays wreak havoc on every organization’s ability to manage time, resources and cash flow.

Short payments can cause negative financial effects on businesses. Unpaid invoices can lead to cash flow issues, which can result in outstanding debt, increased borrowing, or even bankruptcy due to the inability to pay bills or meet financial obligations to vendors, creditors, or even employees.

Also, short payments can negatively impact the relationship between buyers and sellers, leading to possible loss of clients, brand reputation, and the potential legal expenses of recovering unpaid debt. When short payments occur due to errors on your part, it can tarnish your business’ reputation and make future interactions with these customers more challenging.

Finally, the arduous task of identifying the causes behind insufficient payments and resolving disputes consumes valuable time and resources from your financial team. And as we all know, time is a precious commodity they simply cannot afford to waste.

Effects of short payments:

- Reduced cash flow

- Damaged relationships with customers

- Increased administrative costs

The best ways to handle short paid invoices

There is no single solution that will resolve and prevent all short pays from occurring, but there are lots of smart strategies you can use together in order to lessen their impact on your organization. When confronted with a situation involving insufficient payment, businesses can employ a series of steps to address and resolve the issue at hand.

- Analyze: Reporting tools can help you identify short pay trends by reporting on short payment (and overpayment) results to help identify customer service issues as well as allow you to identify customers who continually try to “pull one over on you.” Analyzing this data and passing it on to your sales and billing teams to address the root cause can cut down on these short pays in the future.

- Identify: The next step is to determine the cause of the short payment. Is it an error on your part or a dispute with the customer? Understanding the root cause will help in developing an effective resolution strategy.

- Direct communication: There should always be direct communication with the customer. There may be valid reasons for the short payment that the seller is unaware of. In such cases, a simple conversation can clarify the situation and resolve the issue.

- Review: Gather all relevant paperwork and information, and carefully review the invoice to ensure it matches the agreed-upon contract terms. Errors on the invoice can be resolved quickly, and the remaining amount can then be collected.

- Escalation process: If direct communication and invoice review do not resolve the issue, consider escalating the problem internally within your organization.

- Negotiation: If attempts to resolve the issue through direct communication or escalation fail, consider negotiating with the customer. Offer a discount or other incentives to encourage prompt payments.

- Legal action: If all else fails, legal action can be taken to recover the unpaid amount. However, this option should be used only when all other avenues have been exhausted and is best avoided as it can damage business relationships.

- Follow-up after the resolution: Once the issue is resolved, continue to follow up with the customer. Maintaining open communication and demonstrating a commitment to resolving issues can help strengthen business relationships.

- Preventive measures: To prevent future short payment situations, consider implementing preventive measures, such as detailed contracts and payment terms, accurate electronic invoicing, effective communication strategies, timely reminders, and alternative payment methods.

Short paid invoices are an unfortunate reality for businesses, but they do not have to be a recurring problem. With proper prevention strategies in place and effective resolution processes in case of occurrence, businesses can effectively manage short pay scenarios, reduce their impact on cash flow, and maintain healthy relationships with their customers.

Moral of the story? Don’t be lackadaisical when dealing with these sorts of annoyances. But also, certainly don’t feel like it’s out of your control, either. With a few policies in place, you can minimize the havoc and lost money that short pays and unrecognized deductions can bring.

Speaking of automation…

Your best bet is to start with an invoicing solution or accounting software with customizable deduction codes. These codes will help you reconcile open invoices with short pays faster.

Even better – choose an automated EIPP solution that allows your buyers to pay electronically and use deduction codes which will give you information about their short payment. This type of AR automation software will give you the ability to invoice your customers quickly, and allow them to submit fast payments electronically. Best of all, because the payment and remittance information is linked together, your cash application process will be automated as well.

Want to learn more about how a Billtrust accounts receivable and payments automation solutions can work for you? Take a look at the solutions Billtrust offers.