Finance teams are managing a paradox: Credit is a growth lever and a risk vector. Traditionally, credit management is performed using periodic, spreadsheet‑driven reviews, but these approaches push work to the end of the month, miss early warning signals, and draw capital from the wrong buyers. They can also have cascading effects: late payments, unmanaged risk exposure, and missed revenue from customers who would buy more if they had headroom.

A new operating model for credit management is emerging, thanks to agentic AI. With powerful monitoring capabilities, it can continuously:

- Scan the customer portfolio and identify credit risk

- Highlight where credit line optimization is needed most

- Guide you in making the right credit allocation adjustments

- Explain why those changes are justified

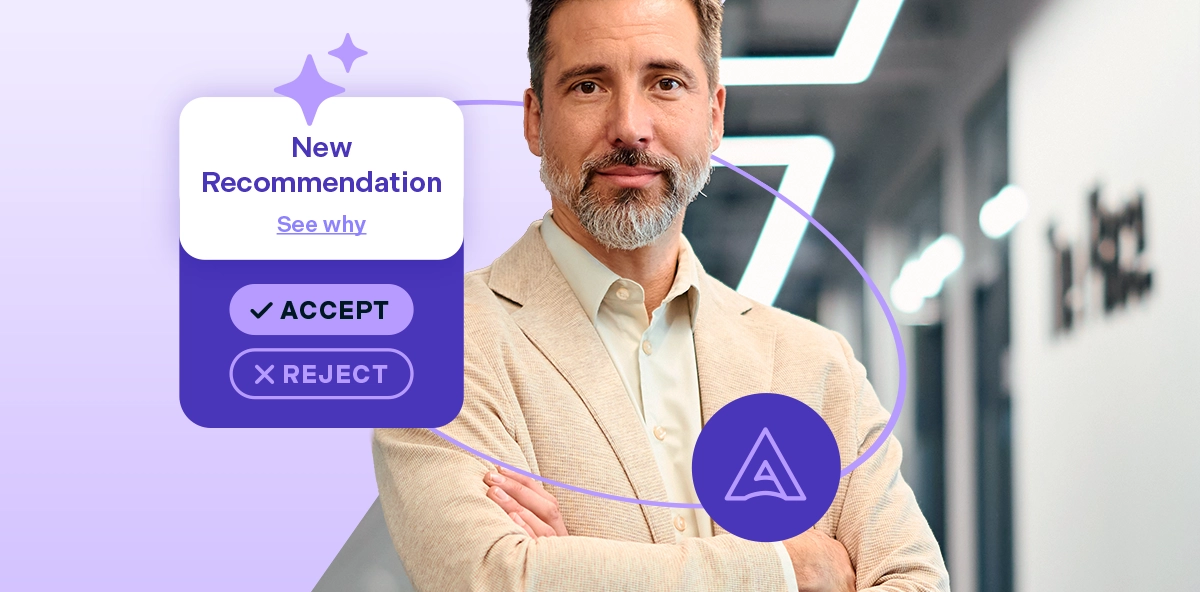

This last point is particularly important, as transparent credit decisioning rationale makes AI automation auditable and more trustworthy. Other key advantages include efficiency and proactive credit risk management. The result? A team that can cover the entire customer portfolio with virtual assistants serving as their credit risk guides. Because every credit adjustment is reviewed, approved, and actually performed by human credit managers – AI supports them, not replaces them.

These are benefits gained from Billtrust’s new Agentic Credit Lines solution: AI‑driven credit recommendations that are trusted due to clear rationale. What’s more? They’re available right where your accounts receivable (AR) team is already working – in Billtrust’s AR automation platform.

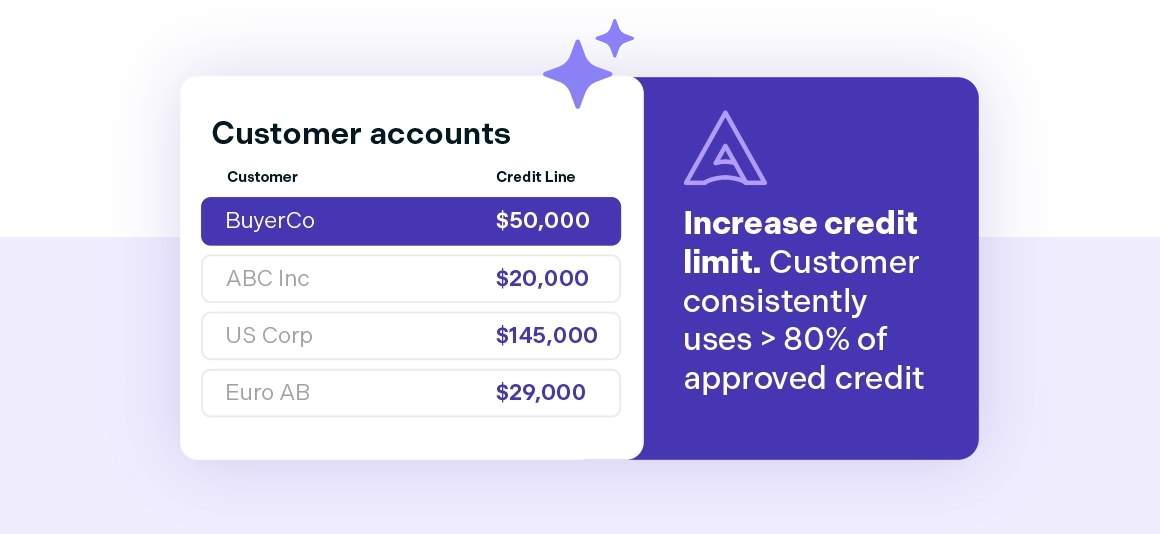

Here’s how it works. Billtrust’s credit management software analyzes 12 months of history, including credit utilization, payment patterns, dispute patterns, and external credit ratings. AI agents use this vast dataset to surface prioritized credit reviews, making recommendations to increase or decrease the customer’s line of credit. Every suggestion comes with auditable explanations conveniently located within existing workflows. Best of all, it even evaluates no‑limit buyers, so financial risk and sales expansion opportunities don’t slip through the cracks.

Key Benefits: Agentic AI for Credit Teams

- Fewer severe delinquencies: In detecting issues earlier, teams can intervene sooner and prevent invoices from aging unnecessarily.

- Wider risk visibility: By combining internal behavior patterns with external signals, organizations gain earlier insight into changes in customer health, enabling proactive action.

- Predictable cash flow: CFOs gain more control over credit decisions, with tighter governance that supports cash flow management.

- Greater efficiency: AR teams don’t need to find data or crunch numbers and can instead focus on prioritized accounts where credit risk is the highest.

Credit Management: More Important than Ever

Late payments are growing problems that heighten the risk of bad debt — and the need for more stringent credit management. According to research published in CFO.com, today’s suppliers are waiting longer for payments to arrive — and the problem is getting worse.

- 31% said their late payments increased over the 12 months

- 32% reported that at least 11% of their invoices are paid late, on average

- 40% said that at least 5% of their annual revenue is lost to bad debt

Industry benchmarking paints a similar picture: Dun & Bradstreet’s AR report shows dozens of U.S. industries where +12% of aging dollars are 30+ days late, a persistent drag that worsens collection effectiveness and forecast accuracy.

Takeaway for CFOs: In a world where economic volatility is constant and payment risk is dynamic, traditional approaches to credit management can’t keep up. When a customer’s financial position changes quickly, annual credit reviews can miss the early signals that constant AI monitoring can catch before delinquency results in bad debt.

5 Signs Your Credit Management Practices are Increasing Risk

- Reactive, narrow coverage: Manual reviews typically cover only a fraction of the customer portfolio (usually large accounts) which leaves quieter risks and emerging issues unnoticed.

- Long application turn-times: Paper‑ and email‑based workflows slow credit decisioning, delay or even block sales orders, and consume scarce time. PYMNTS reports that manual AR processes are a “financial hazard.”

- Periodic reviews: Traditional rules can miss subtle yet ongoing behavior shifts, such as credit utilization spikes, dispute patterns, and late payment signals.

- Rising DSO: Late payments push performance metrics like Days Sales Outstanding (DSO) higher. AI can offset this by reserving credit and putting it where it’s most deserved.

- Inconsistency and audit friction: Inconsistent reviews and allocation criteria create uneven credit outcomes, exposing organizations to financial, regulatory, and operational risks.

What AI-Powered Credit Management Looks Like

AI-powered credit management software gives CFOs what they need: continuous visibility, faster decisioning, and tighter controls they can trust without increasing operational burden. Agentic agents bring these capabilities together by turning scattered data into actionable insight. Across financial functions, automated credit decisioning correlates with earlier warnings and higher efficiency.

- Proactive risk management: continuous monitoring of payment behavior, credit utilization, financial disputes, and external credit signals to flag issues before they hit cash flow.

- Transparency and accountability: each recommendation includes clear, auditable rationale, meeting compliance needs and building trust in automated decisions.

- Portfolio‑wide control: evaluating the data across 100% of buyers, including “no‑limit” accounts, to close gaps in credit risk exposure.

- Speed & efficiency: AI helps prioritize the accounts where humans should focus their attention first, reducing manual triage and time spent deciding what to review and optimize next.

- Revenue generation: identify reliable payors who are also high‑utilization buyers for responsible credit increases that expand purchasing capacity without generating more risk.

92% of finance leaders say AR automation software has helped them effectively mitigate financial and compliance risks. Read the Vanson Bourne research report

Agentic Credit Management: A 5-Step Path for CFOs

- Start with your policy and codify it: Review your credit decisioning rules including the minimum/maximum limits, utilization thresholds, dispute impact, and external score impact. Clarify easy decisions versus human judgement calls, ensuring that even judgement calls can be used to train and modify the way the AI model works.

- Expand your risk visibility: Credit decisioning should be based on both internal and external data. Blend internal signals (payment behavior, open disputes, utilization metrics) with credit bureau data and alternative sources. Widening the field of view enables the early detection of your customers’ financial health deterioration or growth.

- Shift from calendared reviews to continuous optimization: Move reviews from calendar‑driven to signal‑driven. Let AI rank accounts by urgency and financial risk, so analysts spend time on credit line expansions and retractions, not hunting for the next case.

- Focus on transparent decisioning practices: Demand that every AI-generated recommendation comes with an explanation. Every suggested credit line adjustment should show contributing factors (e.g. external credit score +10% QoQ). This shortens approvals and strengthens audit processes.

- Treat credit as a growth instrument: Leverage AI to find new sales opportunities — reliable payors who frequently hit their limits. Increase credits lines to support revenue while also maintaining real‑time monitoring through automation.

Before You Go…

CFOs, controllers, and credit managers don’t lack discipline. They lack time. Manual reviews can’t see enough data fast enough. The shift to agentic AI turns credit oversight from a periodic, error‑prone chore into a continuous, decisioning powerhouse. In the end, financial leaders never have to get caught in the paradox — credit as a growth lever but alsoa risk vector. Instead, they can balance the tradeoffs, both funding business growth while preventing bad debt.