Poland: No mandatory KSeF in 2024

The Ministry of Finance has decided to postpone the date of entry into force of the mandatory National e-Invoicing System (KSef) which would have been mandatory from July 1st, 2024. Because of problems related to the code, functionality and efficiency of the system, KSeF will not be rolled out in 2024. A new date of entry into force of the KSeF will be presented after the system audit.

At the end of 2023, the Polish Ministry of Finance had run public consultations on two changes to KSeF. Taxpayers could comment on a couple of changes to KSeF.

The first draft, on the technical regulation for KSeF, implied the following:

- QR code generating for invoices that are used outside of KSEF

- Offline invoicing: the access to invoices issued in the event of systems failure and/or unavailability of the KSeF system

- New types of KSeF authorizations and authentication methods

- Scope of data for VAT RR invoices (applicable to the special procedure for entities buying crops from farmers) and correcting VAT RR invoices

The second draft was related to the amendment on issuing invoices:

- As of January 1, 2025, tax exempt taxpayers have the obligation to include the NIP of the buyer and the seller on KSeF invoices.

- A simplification for continuous services transactions (e.g. supply of utilities). An invoice may not contain measurement and quantity of goods delivered – or scope of services provided – and the unit price without tax (net unit price).

Taxpayers had until December 18 to provide comments on both drafts. The existing technical regulations regarding using KSeF – the regulation of December 27, 2021 on the use of the National e-Invoice System – expire on June 30, 2024. The proposed regulation will specify new rules for using the mandatory KSeF and will apply to all taxpayers using the KSeF.

| Timeline | Targeted Organizations |

|---|---|

| 2025* | B2B e-invoicing mandatory for all VAT-registered Polish entities and Polish branches of foreign entities. |

* Timeline decided after system audit, subject to change.

Germany: decision on B2B e-invoicing expected in 2024

In Germany, mandatory B2B e-invoicing is part of a broader regulatory reform called the Growth Opportunities Act, which consists of a total of around fifty fiscal policy measures including mandatory e-invoicing for B2B transactions.

Although there was a push to get the Growth Opportunities Act approved before Christmas, on November 17, 2023 the Bundesrat (federal council) rejected the Growth Opportunities Act in the version revised by the Bundestag (federal parliament). The Bundestag was seeking a compromise 1-year extension for the full e-invoicing. The Bundesrat was seeking a 2 year delay, to January 2027.

As a result, an agreement was to be reached in a mediation process between the federal and state governments at the beginning of December 2023. On December 8, 2023, the informal working group set up by the federal and state governments broke off its consultations on the contentious points of the Growth Opportunities Act without a result. The mediation committee convened by the Bundesrat will therefore not meet again this year.

Negotiations between the federal and state governments on the provisions of the Growth Opportunities Act are to continue at the beginning of next year. A further splitting of the Act into individual contents is currently being discussed, which could then be transferred to other legislative procedures. This particularly concerns the tax law adjustments in connection with the Act on the Modernization of Partnership Law (“MoPeG”), which comes into force on January 1, 2024.

| Timeline* | Targeted Organizations |

|---|---|

| Jan 1, 2025 | All companies are obligated to send and receive e-invoices. However, trading partners are still allowed to exchange PDF or paper invoices if both parties agree. |

| Jan 1, 2027 | All companies over 800k EUR revenue are mandated to send e-invoices. |

| Jan 1, 2028 | All companies are mandated to send e-invoices. |

* Last known timeline, subject to change.

Belgium: Mandatory B2B e-invoicing in 2026

In Belgium, a preliminary draft law, making B2B e-invoicing mandatory, was approved on the 29th of September 2023. The preliminary draft law is now going through federal government revision before it will be published as draft law to the Belgian parliament (and becomes publicly available).

On December 8, 2023, the council of Ministers approved the preliminary draft law in second reading requiring the use of structured electronic invoices. The draft law is submitted to the King for signature, with a view to its submission to the House of Representatives.

| Timeline | Targeted Organizations |

|---|---|

| Jan 1, 2026 | All taxpayers will have to issue, exchange and receive invoices electronically.

For now, electronic reporting is not mandatory but will take place at a later stage. |

Malaysia: e-invoicing framework from 2024

The Malaysian Peppol Authority MDEC plans to have an interoperable e-invoicing framework in place by early 2024. Technical guidelines suited to local requirements target to be ready by the end of 2023 and will be published on the MDEC website.

| Timeline | Targeted Organizations |

|---|---|

| Aug 1, 2024 | Mandatory e-invoicing for businesses with an annual turnover of MYR 100 million and more. |

| Jan 1, 2025 | Mandatory e-invoicing for taxpayers for businesses with an annual turnover of more than MYR 25 million and up to MYR 100 million. |

| July 1, 2025 | Mandatory e-invoicing for all businesses |

Spain: SIF certified electronic Invoicing expected to come into effect as of July 2025

Spain has issued a Royal Decree that outlines the rules on invoices and their electronic production, including computerized invoicing. This covers certified invoicing systems and voluntary submission of invoices to the Agencia Tributaria – sistemas y programas informáticos o electrónicos (‘SIF’). The regulations are applicable for companies that are not subject to the current SII reporting obligation.

It is essential to note that the aforementioned regulation does not pertain to B2B e-invoicing. The regulation regarding the e-invoicing mandate is still pending approval in the Spanish government and is anticipated to be implemented in Q1 or Q2 of 2025 for large taxpayers. However the go-live dates are not yet confirmed.

| Timeline | Targeted Organizations |

|---|---|

| Q1/Q2 2025 | For taxpayers with an annual turnover of €8M and more. |

| 2026 | For all other companies and professionals. |

Romania: CTC obligation on its way

Starting January 1, 2024 all domestic B2B & B2G invoices (detailed at line level) issued where the place of supply is in Romania must be reported to the tax authorities in the RO e-factura system within 5 working days from the date of issuing the invoice. There is a grace period of sanctions for failure to timely report between January 1, 2024 and March 31, 2024. This is applicable to both established and non-established companies with a VAT registration in Romania.

Also, starting in July 2024, Romania will be implementing a clearance method whereby domestic B2B e-invoices must undergo validation by the tax authority before they can be transmitted to the customer. It will be mandatory to issue electronic invoices in an XML format via the RO e-factura system. On the accounts payable (AP) side, taxpayers must retrieve the e-invoices from the RO e-factura system for the domestic acquisitions from established entities. Mandatory e-invoicing is applicable to established legal entities only whose e-reporting obligations (mentioned above) will be replaced by the e-invoicing obligation.

| Timeline | Targeted Organizations |

|---|---|

| Jan 1, 2024 | B2B and B2G domestic e-reporting mandatory |

| July 1, 2024 | Domestic B2B e-invoicing mandatory for all companies via RO e-factura system |

An introduction to e-invoicing in Mexico

Mexico has been at the forefront of digital tax transformation in Latin America, pioneering the implementation of mandatory e-invoicing for all taxpayers since 2014. This progressive step has streamlined tax compliance processes, enhanced data integrity, and fostered a more transparent business environment.

The SAT (Servicio de Administración Tributaria), Mexico’s tax administration agency, plays a crucial role in facilitating e-invoicing. Its electronic services are mandatory for issuing invoices and other accompanying receipts. Additionally, the SAT has delegated the verification of electronic invoices to certified Public Accounting Service Providers (PACs).

To ensure timely tax information exchange, the issuer is obligated to communicate the invoice to the recipient within three days following issuance, while buyers can ask for a printed copy.

To safeguard the integrity of electronic invoices, Mexico employs a rigorous signing and “timbrado” process. The supplier’s CSD (Certificado de Sello Digital), a certificate issued by the tax authorities, authenticates the invoice. It journeys to an authorized PAC for validation and compliance with XML format standards, and receives a unique identifier (UUID). The PAC then signs the invoice with the key provided to the tax authority, completing the timbrado process. The result is returned to the supplier, or service provider.

The PAC also places a Digital Seal to authenticate the CFDI (Comprobantes Fiscal Digital por Internet), ensuring the invoice’s origin and legitimacy. Both the issuer and the recipient must maintain their respective Digital Seal Certificates (CSD) up to date. If the SAT suspends these certificates due to tax delinquency or other reasons, the generation of tax receipts is prohibited.

Latest updates on ViDA

With the VAT in the Digital Age (ViDA) proposal, the European Commission wants to modernize the EU’s Value-Added Tax (VAT) system. A new real-time digital reporting system based on e-invoicing is part of it and will impact the way invoices will be exchanged between businesses, organizations and governments.

One of the main goals of ViDA is to help EU Member States collect more in VAT revenues annually and address the VAT gap that is occurring today. According to the latest report from 2021, the 27 Member States lost around €61 billion in missing VAT, a notable decrease from the 2020 figure of €99 billion.

How will ViDA impact invoicing?

- All intra-community transactions would need to be reported to a centralized European Digital Reporting system.

- ViDA would allow EU member states to introduce mandatory e-invoicing for domestic transactions without having to get special permission (‘derogation’) from the EU.

Hopes for harmonization

The negotiations between the European Commission and its member states on the ViDA proposal are not progressing swiftly. From an e-invoicing and e-reporting perspective it is our understanding that the negotiations are hindered by the fact that there are large differences between the member states.

In July 2017, Spain implemented near real-time transaction-based reporting, followed by Hungary in July 2019. Italy mandated e-invoicing in January 2019, and ongoing efforts in Romania, Poland, and France are paving the way for mandatory e-invoicing in these countries.

There is a collective aspiration among those advocating for a more unified European e-invoicing landscape that Belgium, assuming the role of the next President of the Council of the European Union from January to the end of June 2024, will place priority on the ViDA proposal and work towards achieving consensus among the member states.

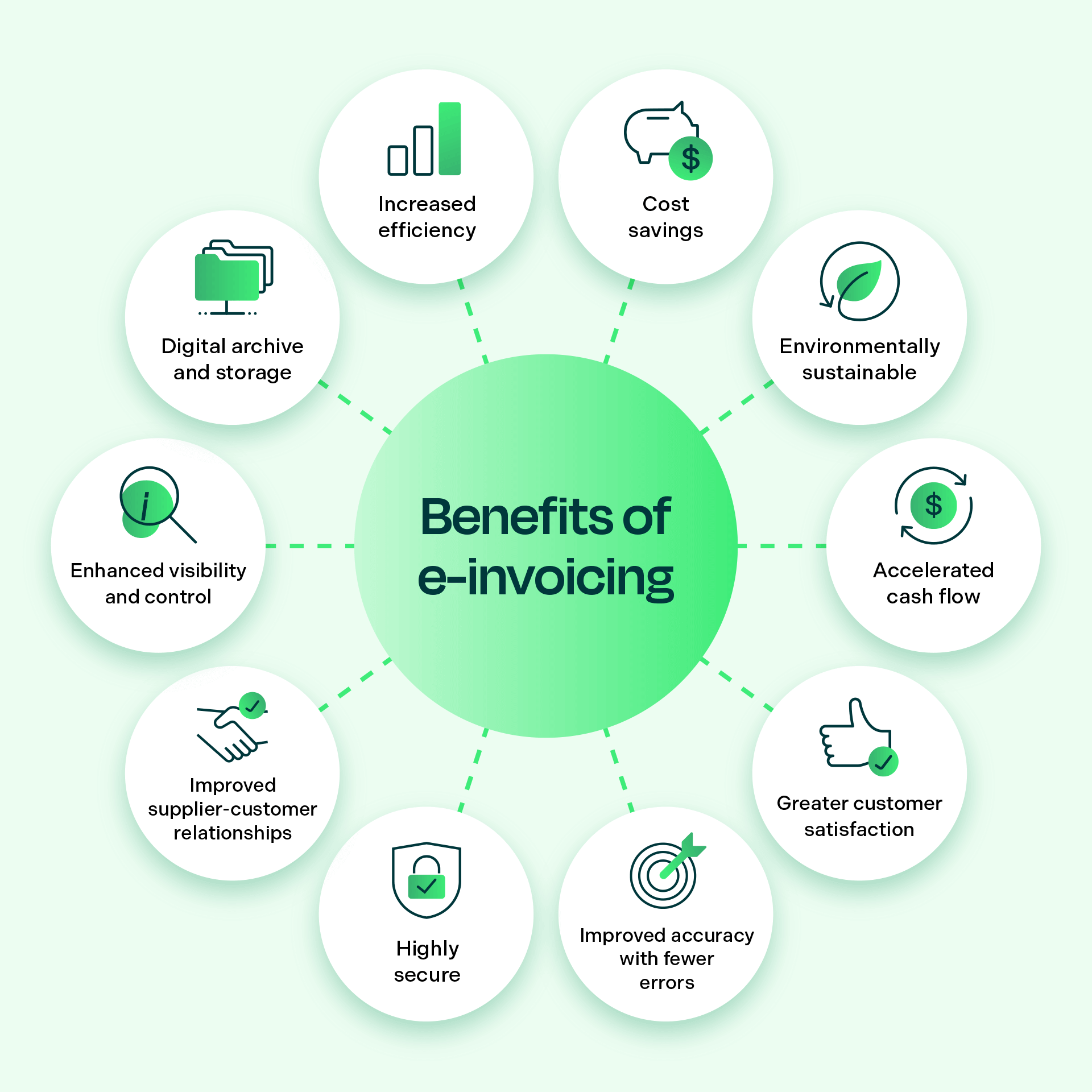

Going paperless — and more — with e-invoicing

If you are looking for a way to improve your business’s financial processes, e-invoicing is a great option to consider. It offers a number of benefits, including cost savings, increased efficiency, improved accuracy, improved security, and compliance. E-invoicing can also help your business improve cash flow, customer satisfaction, visibility and control, and environmental sustainability.

Want to learn more about mandatory e-invoicing? Read our report E-invoicing interoperability and compliance.

The information presented and timelines provided are accurate as of the date of publishing. Due to the dynamic nature of regulations and legislation, these timelines may change accordingly.