This post was originally published in Oct 2024 and was updated in August 2025 with additional information on why AR scams are evolving, FAQs, and more.

No matter how many ways finance teams try to fight fraud, bad actors always devise new accounts receivable scams. According to the 2025 AFP® Payments Fraud and Control Survey, 79% of organizations were victims of payments fraud attacks or attempts in 2024. Only 22% of those were able to recover 75% or more of the funds lost due to payments fraud.

It doesn’t have to be a losing battle with a strong payment fraud prevention strategy. Even if you can’t stay on top of every new scam that emerges, there are some telltale signs that scams typically have in common.

Read the blog → Accounts receivable fraud: How to detect and deal with it

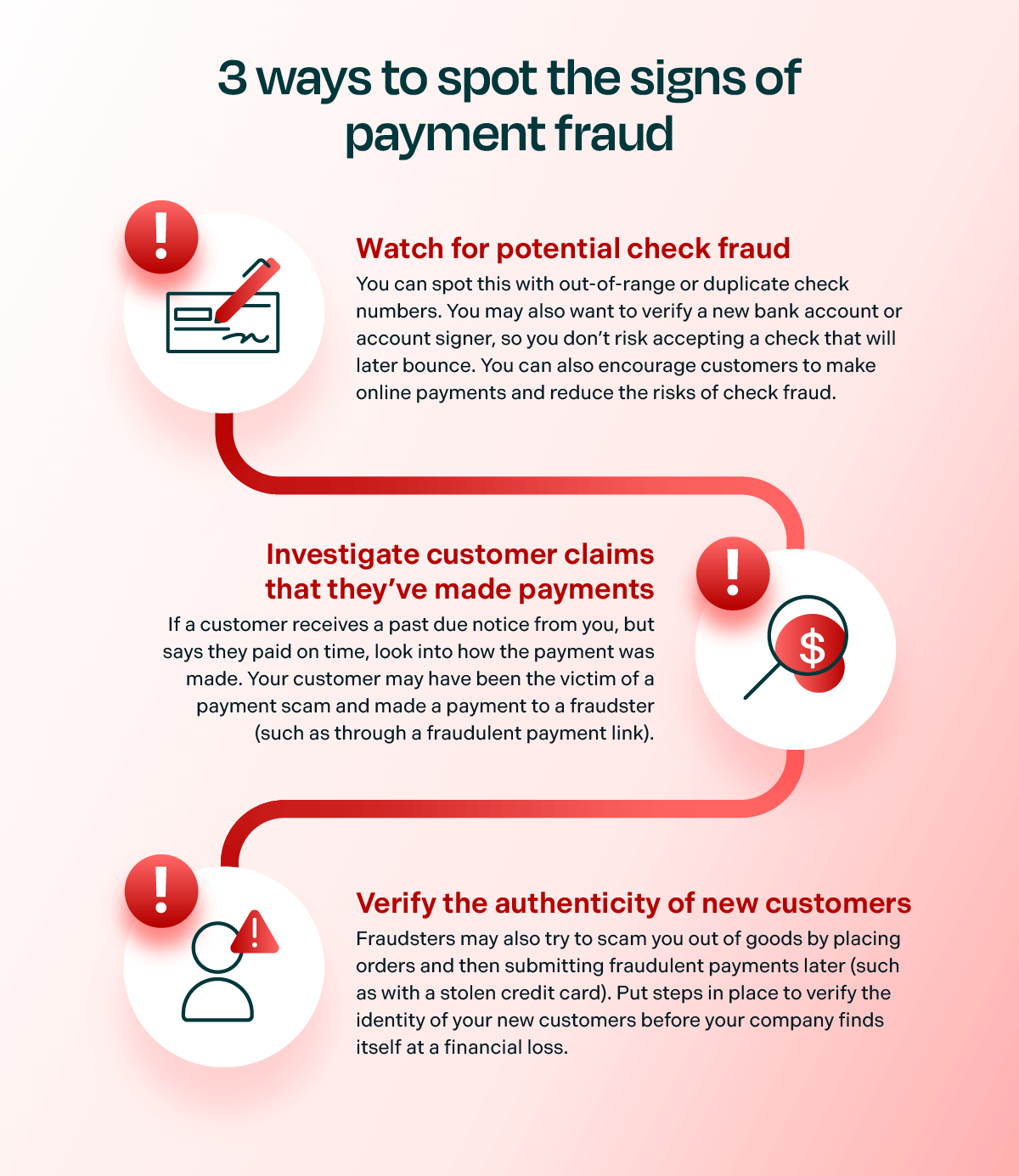

3 ways to spot the signs of payment fraud

Fraudsters will try to scam payments in several different ways. Checks, for example, are a frequent target. Additionally, your organization may be a target of payment fraud in other ways, such as a fraudster intercepting your customers’ payments or the customers themselves being fraudsters.

- Watch for potential check fraud. You can spot this with out-of-range or duplicate check numbers. You may also want to verify a new bank account or account signer, so you don’t risk accepting a check that will later bounce. You can also encourage customers to make online payments and reduce the risks of check fraud.

- Investigate customer claims that they’ve made payments. If a customer receives a past due notice from you, but says they paid on time, look into how the payment was made. Your customer may have been the victim of a payment scam and made a payment to a fraudster (such as through a fraudulent payment link).

- Verify the authenticity of new customers. Fraudsters may also try to scam you out of goods by placing orders and then submitting fraudulent payments later (such as with a stolen credit card or credit card information). Put steps in place to verify the identity of your new customers before your company finds itself at a financial loss.

How modern fraud tactics are targeting your accounts receivable

As a finance leader, you’re facing a rapidly changing threat landscape. Accounts receivable scams in 2025 aren’t just more frequent—they’re fundamentally different. Traditional fraud tactics now combine with technology, making them harder to detect and potentially more damaging to your cash flow and customer relationships. Your finance team can no longer rely on reactive approaches to fraud detection. Building proactive defenses into your AR processes has become essential for protecting your organization.

Factors making AR fraud more prevalent and sophisticated

Several key trends are creating new vulnerabilities in your accounts receivable operations:

- Digital payment acceleration: As your organization moves payments and invoicing online, cybercriminals are targeting digital weak spots—particularly in legacy AR systems that may lack security features.

- AI-enhanced fraud techniques: Fraudsters use AI to mimic legitimate customer behavior, generate convincing phishing content, and bypass traditional rule-based detection systems your team may rely on.

- E-invoicing transitions: While e-invoicing standards improve transaction security, the implementation period creates process gaps that scammers exploit to intercept or redirect your payments.

- Sophisticated impersonation fraud: Scammers can convincingly imitate your vendors, customers, or even internal employees to redirect payments or submit false invoices to your organization.

Why yesterday’s fraud prevention isn’t enough for today’s threats

Modern AR fraud presents unique challenges that require updated detection strategies:

- Speed of execution: Bad actors exploit real-time payment systems, giving your team little time to intervene once a fraudulent transaction begins.

- Automated scale: Bots and scripts enable mass fraud attempts against your organization with minimal human effort from criminals.

- Pattern mimicry: Scammers often replicate behavior that matches your expected customer patterns, making manual reviews less reliable for your AR team.

- Multi-channel complexity: A single fraud attempt may start with a phishing email, continue through a fake portal, and end in a fraudulent ACH transfer—all designed to look like normal business activity.

These evolving tactics mean your traditional fraud detection methods—manual reviews, standard policies, and paper trails—need to be enhanced with more sophisticated, technology-driven approaches.

Be on the lookout for email scams

Email scams can compromise your customers—and hurt your business—in a few different ways. Business email compromise (BEC) is a common type of payment scam where a fraudster impersonates a company to trick businesses or consumers into changing their payment information. Your customers think they’ve made a payment when the money has actually gone into the fraudster’s bank account.

Business email compromise (BEC) remained the No. 1 avenue for attempted and actual payments fraud in 2024, cited by 63% of respondents. Spoof emails were the most prevalent type of BEC, cited by 79%. (2025 AFP Payments Fraud and Control Survey Report)

Scammers may also try to target your company through a phishing scheme. If someone on the finance team shares sensitive information, it can expose you to a cybercrime that puts your customers at risk.

- Make sure your customers know how to identify emails from your company. This reduces the risk that your customers fall victim to a BEC scam. You can also streamline invoicing your customers through Billtrust’s portal processing, and avoid emailing invoices altogether.

- Make sure your team knows how to identify phishing schemes. These emails often have suspicious links or request “immediate action.”

Keep track of what’s normal to detect unusual activity

One of the best defenses against fraud is to know what “normal” activity looks like for your customers. The sooner you spot something unusual, the sooner you can stop scams from harming your company or customers.

For example, a manufacturing company may notice a sudden increase in orders from a supplier, which could indicate unauthorized activity. The company may also notice excessive chargebacks, indicating that scammers are trying to get goods without paying for them.

Don’t forget about internal controls

While a lot of scams happen externally, you can’t ignore that fraud can happen within the company as well. An employee may create fake invoices so they can divert payments into their own account, or initiate write-offs to cover up theft.

If someone on the finance team suspects another employee of a scam, make sure they know how to report it. You should also look for employees who don’t want to take time off or are unwilling to train others. They might be worried that their scam will be discovered if someone else can access their work. Set up as many dual controls as possible.

Technology can minimize risks

If everyone on the finance team has to keep their eyes on everything, scams may still slip through the cracks. Fraudsters are betting that people simply can’t keep up and still get their daily work done.

Data analytics, AI, and machine learning can spot these patterns and help you better manage your risk. While the best defense in the fight against accounts receivable scams and payment fraud is your own finance team, automation tools can give them the time to identify possible fraud. From spotting anomalies to recognizing customers’ past payment activity, technology can sift through large amounts of data and alert you to issues needing your attention.

For more on AR fraud, read → “15 types of accounts receivable fraud (and how to detect and prevent them)”.

Taking action to safeguard your AR operations

The financial impact of AR fraud on your organization is no longer a hypothetical risk. A successful scam can disrupt your cash flow, damage customer relationships, and harm your company’s reputation.

As a finance leader, you need to build a response plan to handle potential fraud incidents effectively:

- Clear reporting protocols: Establish straightforward procedures for how your employees should report suspected fraud attempts, including designated contacts and escalation paths.

- Defined response workflows: Assign specific responsibilities for initial review, investigation, and escalation to ensure your team responds quickly and consistently.

- Prepared customer communications: Develop pre-approved messaging templates to communicate with affected customers professionally and transparently.

- Internal coordination processes: Define when and how to involve your legal, audit, or risk management teams to ensure appropriate oversight.

Without a structured response plan, your organization may experience delays in addressing fraud attempts, potentially missing critical signals and increasing your financial exposure.

Integrate payment fraud prevention into your AR operations

The most effective fraud protection measures have security built directly into your accounts receivable processes rather than layered on top. When evaluating AR platforms, look for integrated capabilities that include:

- Real-time detection: Systems that can identify unusual patterns in customer behavior or payment activity as they occur.

- AI-powered behavior analysis: Technology that learns normal customer patterns and flags deviations that may indicate fraudulent activity.

- Automated verification tools: Built-in processes for validating customer information and payment details before processing.

- Integrated alert systems: Fraud notifications that appear directly within your AR workflow dashboards, enabling immediate action.

By embedding security capabilities into your AR operations, you eliminate the gaps and delays that fraudsters often exploit to target your organization.

Strengthen your fraud prevention with Billtrust’s AR platform

Billtrust’s unified AR platform helps you detect and prevent fraud before it impacts your cash flow and customer relationships. Our integrated approach combines AI-driven insights, secure customer portals, and automated invoice-to-cash processes to help you:

- Monitor suspicious activity: Flag unusual behavior patterns in real-time across your entire customer base.

- Reduce email-based fraud exposure: Minimize risks through secure payment methods that eliminate fraudulent email interception.

- Maintain strong internal controls: Enforce role-based access and approval workflows to prevent internal fraud attempts.

As fraud tactics continue to evolve, having scalable technology integrated into your AR operations provides the proactive defense your organization needs. Connect with our team to learn how Billtrust can enhance your fraud prevention strategy.