For CFOs operating in the EU, VAT has always been a retrospective headache. Historically, businesses reported transactions months after they happened, but the era of the “look-back” task is over.

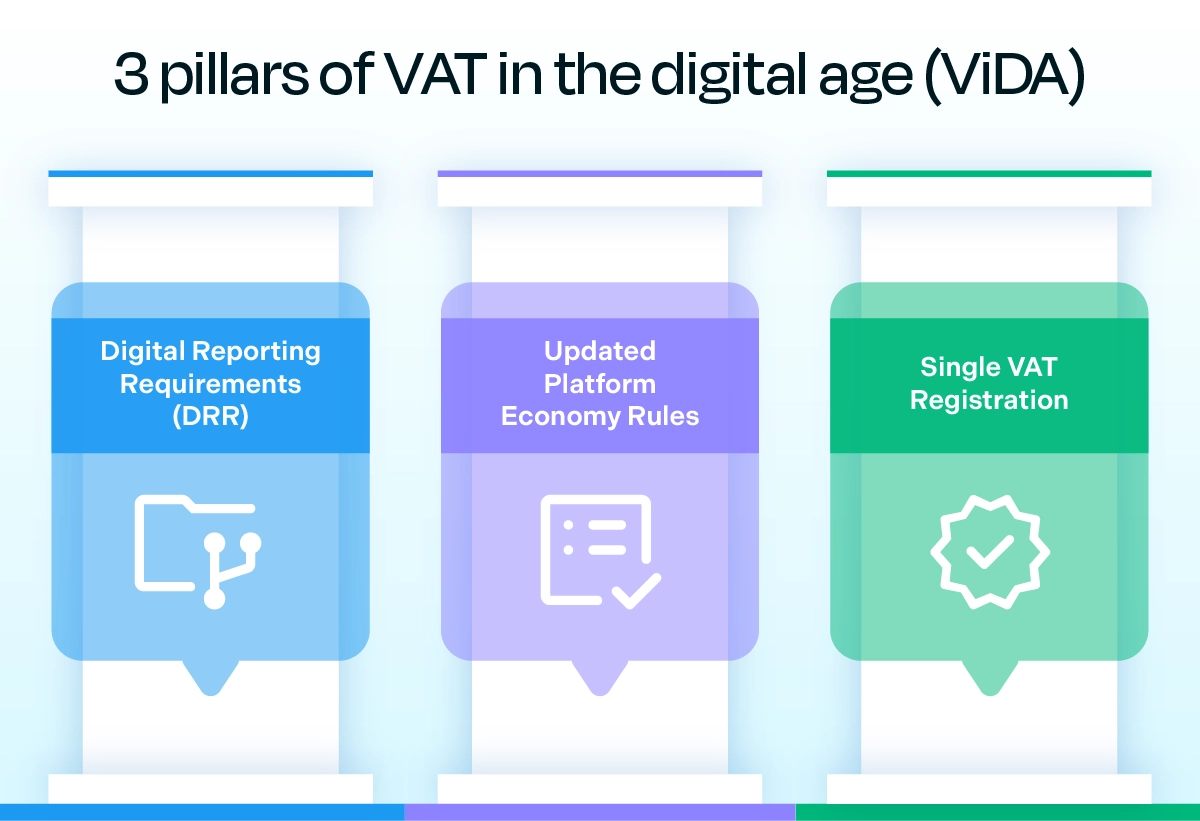

The EU’s VAT in the Digital Age (ViDA) package is a total overhaul of how you’ll invoice, report, and manage VAT. We are moving from periodic reporting to near real-time transparency. It is the biggest shift in the system since its inception, and while the 2030 deadlines feel far away, the clock officially started ticking with the legislation’s adoption in 2025.

Here are the 5 realities you need to know to protect your operations and your bottom line.

ViDA: 5 Fast Facts for Meeting 2030 Compliance Deadlines

Fact 1: The Deal is Done. ViDA is Officially Here.

The Reality: After extensive debate and negotiation, the ViDA compliance package was formally adopted by the EU Council on March 11, 2025 and has entered into force as of April 2025. What was once a series of ambitious proposals has now been enshrined in EU law, establishing a clear and mandated timeline for implementation.

Why This Matters to You: This closure removes any lingering uncertainty. The countdown to mandatory compliance has officially started, You can no longer defer budget allocation or strategic planning. ViDA is now an unavoidable reality for your business.

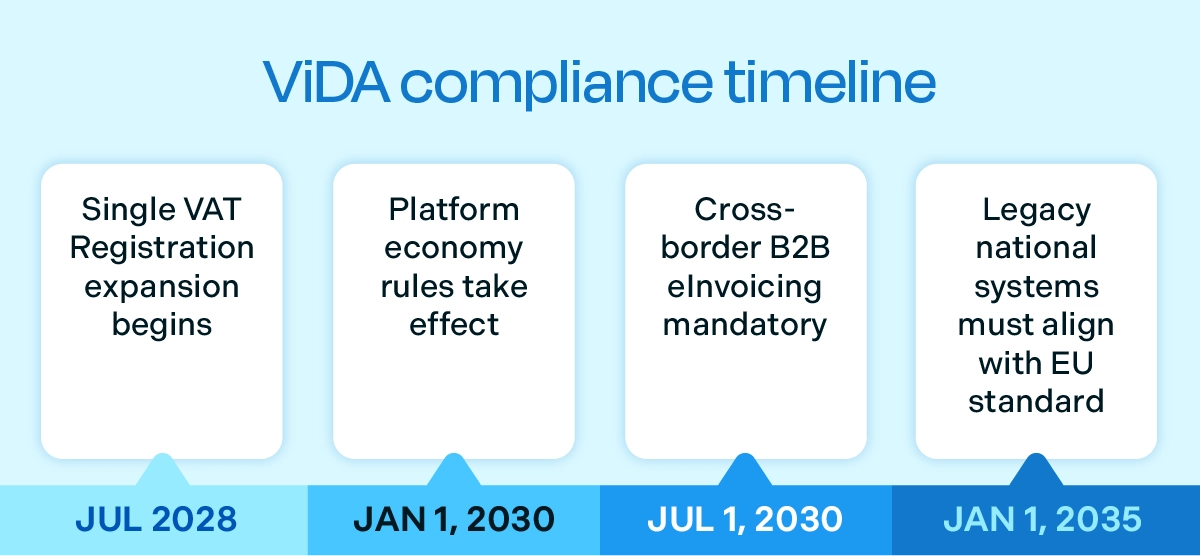

Key Deadlines at a Glance:

- July 2028: Single VAT Registration expansion begins

- January 1, 2030: Platform economy rules take effect

- July 1, 2030: Cross-border B2B eInvoicing mandatory

- January 1, 2035: Legacy national systems must align with EU standard

Closing the Tax Loopholes

ViDA introduces the “Deemed Supplier” rule and “Platform Economy” rules. If your business model relies on a digital platform — think online marketplaces or ride-hailing apps — you will now assume full responsibility for collecting VAT. Previously, portions of these transactions went untaxed. The new rules close this gap, ensuring VAT is collected on the full price paid by the consumer.

Fact 2: The PDF Invoice is Dead. You Need the New Standard.

The Reality: On July 1, 2030, the traditional Recap Statement (EC Sales List) will be abolished. Its replacement? Comprehensive Digital Reporting Requirements (DRR) for all B2B transactions between EU Member States.

Why This Matters to You: This effectively kills the PDF invoice for cross-border EU trade. Sending a PDF or a non-compliant XML will no longer constitute a legally valid invoice. Furthermore, the data from these eInvoices must be reported to the relevant tax authorities in near real-time, providing an almost immediate overview of cross-border trade.

If your ERP system’s data is incomplete (missing IBANs or Due Dates), your invoices will fail validation, directly impacting your cash flow. You must adopt the European Standard (EN16931).

The New Rules of Engagement:

- Real-Time Reporting: Invoice data is transmitted to tax authorities instantly.

- 10-Day Window: Suppliers must issue the invoice within 10 days of the supply.

- 5-Day Reporting: Buyers must report the transaction within 5 days.

- The Audit Trap: The EU’s new Central VAT Information Exchange System (VIES) database automatically matches seller reports against buyers reports. Any discrepancy triggers an immediate audit flag.

What is EN16931?

Think of it as the common language all EU tax systems will speak from 2030 onward. It ensures that eInvoices can be understood and processed across all EU Member States, regardless of the technical format (XML, JSON, etc.) used to transmit them. Think of it as the common language that all EU tax systems will speak from 2030 onward.

Pro Tip on Invoice Formats: The legislation explicitly supports Hybrid formats (like Factur-X). This allows you to send a single file containing both a human-readable PDF and machine-readable XML data — perfect for bridging the gap between your IT systems and your Accounts Payable team.

Fact 3: Expect a Surge in National Mandates

The Reality: A significant change effective April 2025 removes the requirement for EU Member States to obtain special permission to introduce mandatory B2B eInvoicing.

Why This Matters to You: This potentially triggers a regulatory domino effect. Expect a rapid acceleration of national eInvoicing mandates across the EU between now and 2030. Countries like Germany and France can now press ahead without delay.

If you operate across multiple EU countries, you will likely face a patchwork of differing national requirements well before the 2030 deadline. Monitoring individual country initiatives is now a critical finance function. Check out the latest eInvoicing compliance update.

Proactive monitoring of individual country initiatives is crucial, and Billtrust’s resources can help. Watch our blog for quarterly eInvoicing updates and explore the eInvoicing compliance map for country-by-country breakdown.

Good News for Early Adopters: Worried about your existing investments in Italy (SdI) or Poland (KSeF)? Rest assured, your efforts will be rewarded. Countries with pre-2024 domestic systems have a grace period until January 1, 2035. You have a 9-year runway before you must align those legacy connections with the EU standard.

Fact 4: Two Wins for Finance Operations

The Reality: The final ViDA text includes two critical concessions that safeguard operational efficiency: the removal of “Buyer Consent” and the survival of “Summary Invoices.”

Why This Matters to You:

- No More Buyer Consent: You can now unilaterally switch to eInvoicing without chasing consent forms from every customer. This allows you to shut down print and mail centers faster.

- Summary Invoices Survive: You may continue to group multiple shipments into one monthly invoice (provided it is reported by the 10th of the following month). This prevents the nightmare of issuing millions of individual transaction invoices.

Fact 5: The Silver Lining. How ViDA Cuts Your Costs.

The Reality: ViDA expands beyond just invoicing to fundamentally change who collects tax and where you register.

Why This Matters to You: This drastically simplifies EU logistics.

- Single VAT Registration: From July 1, 2028, the “One Stop Shop” (OSS) expands to cover the transfer of your own inventory between EU countries.

- The Benefit: Currently, moving stock from Belgium to France often triggers a requirement to register for VAT in France. The new rules eliminate this, allowing you to de-register local VAT IDs and manage everything from a single portal.

- Deemed Supplier: Starting January 1, 2030 (with an optional phase from July 2028), platforms in short-term accommodation and passenger transport become the “Deemed Supplier.” For instance, if an Airbnb host isn’t VAT-registered, Airbnb itself becomes responsible for the VAT.

The Road Ahead: Data is Your Greatest Asset for ViDA Compliance

More than just tax compliance, ViDA requires you to fundamentally rethink how you capture, structure, and share transaction data. The ability to report structured invoice data in near real-time is now non-negotiable.

Start your preparation now:

- Audit existing ERP systems for EN16931 compatibility.

- Validate data quality (specifically IBANs and VAT IDs).

- Identify partners and AR automation software that support the EN16931 standard

- Train finance and IT teams on the new structured data requirements

If you need a personal consultation, don’t hesitate to reach out to one of Billtrust’s global invoicing experts.