This post was originally published in October 2021 and was updated in July 2025 with additional information on how remote deposits work, FAQs, and more.

What are remote deposit services and how do they work?

Remote deposit services let businesses deposit checks without visiting a bank branch, which helps finance teams maintain steady cash flow. This technology uses mobile apps and scanning equipment to capture check images that get submitted through banking platforms.

For AR teams, remote deposits mean your staff can photograph checks with smartphones or use desktop scanners to process payments. The convenience sounds appealing, but these services often create unexpected complications for accounts receivable operations that need thoughtful solutions.

Download our tip sheet → Achieve industry-leading match rates with AI-powered cash application

Let’s address the elephant in the room: cash application

Many firms are surprised to hear that remote deposit acceptance significantly slows down their cash application process. This is a huge problem for AR teams because cash application is often the most time-consuming activity of most AR departments.

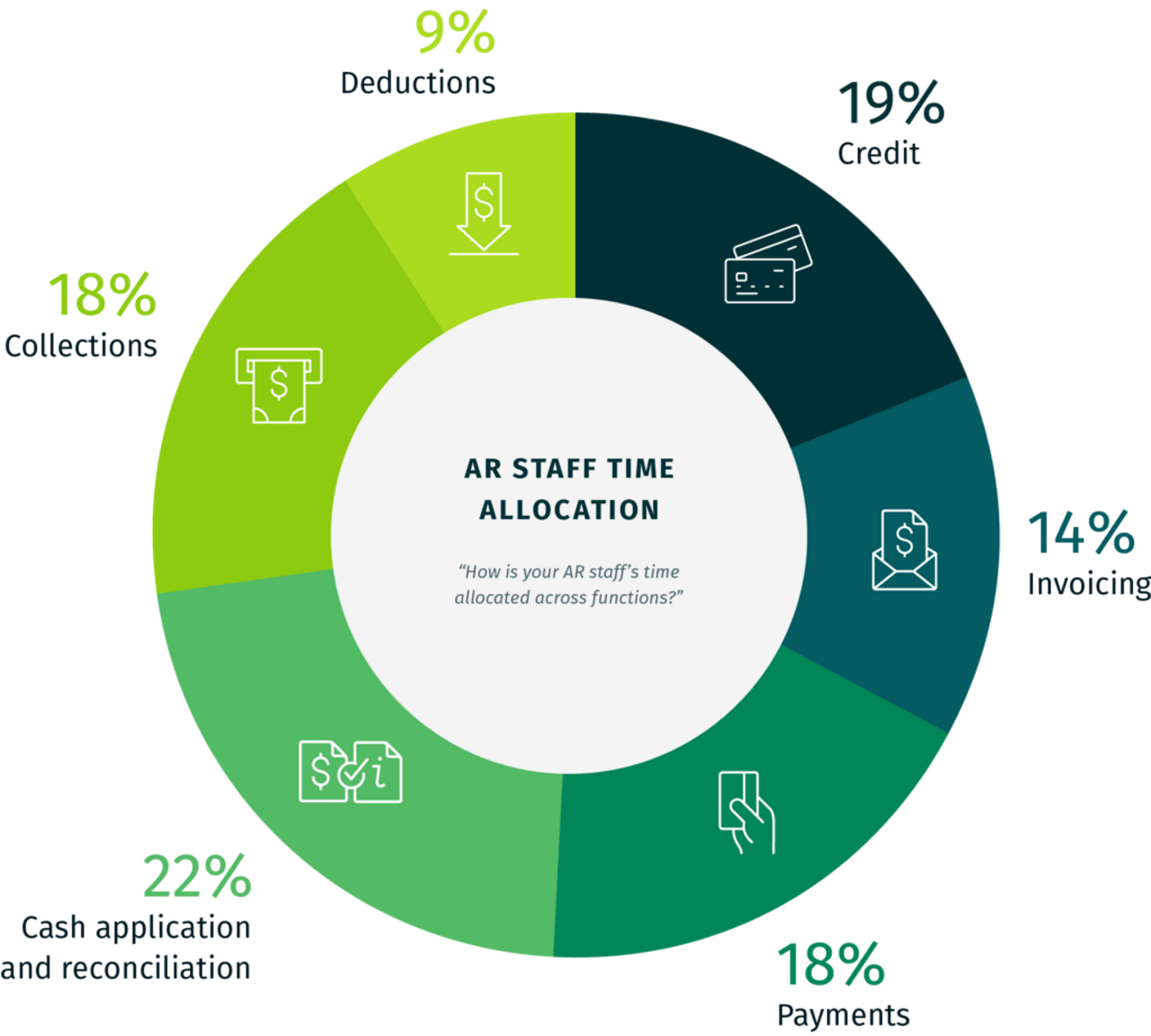

How AR staff allocates their time

Did you know AR departments spend 22% of their time on manual cash application, making it more tedious than handling credit application, invoicing, payments, collections and deductions? This time drain becomes even more pronounced when remote deposits enter the equation, creating additional layers of complexity that slow down an already labor-intensive process.

Behind the curtain – remote deposits slow down cash application

Why is cash application so time-consuming? A key culprit for long cash application processes is how efficiently, or inefficiently, your staff is handling remote check deposits. Let’s face it. Remote check deposits are time-consuming and difficult to process for a variety of reasons – checks are often lost, and cash from checks is only available once you make weekly trips to the bank.

Below, we will investigate the root causes of inefficient remote deposit acceptance and explore best practices to reduce your time to post remote deposits, empower field staff to process checks faster, and automate cash application for your AR team.

Common types of remote deposits

To understand the root causes of inefficient remote deposit acceptance, we must first look at the two major types of remote deposits: branch payments and field payments.

Branch payments are typically dropped off at a local branch and scanned for deposit via a desktop application with high performance scanners such as those manufactured by Digital Check. On the other hand, field payments are checks received in the field or at your customer’s location.

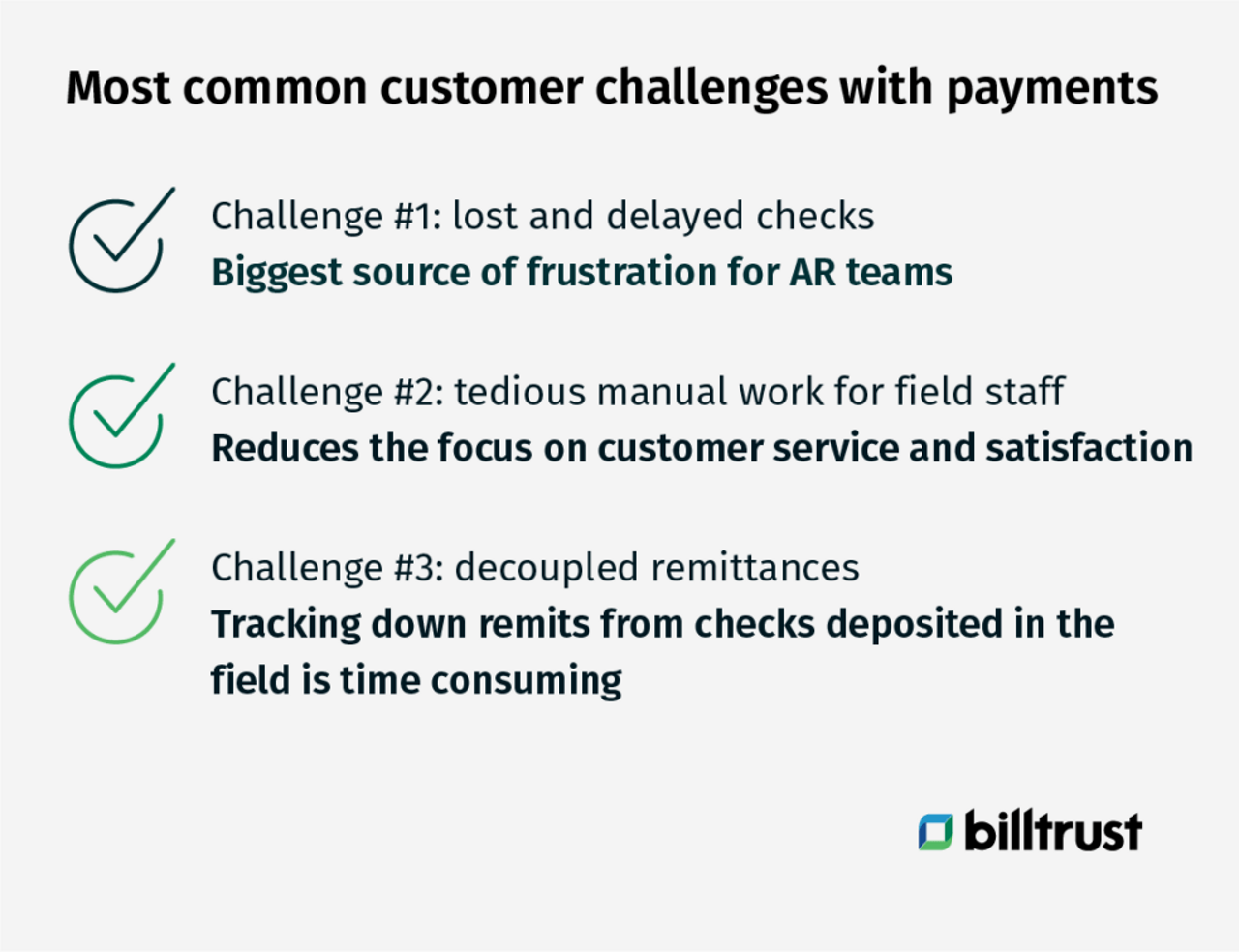

Most common customer challenges with payments

Let’s focus on solving the three most widespread challenges associated with field payments: lost/delayed checks, tedious manual work for field staff and decoupled remittances.

Challenge #1: Lost and delayed checks

The biggest source of frustration for many AR teams is lost revenue from checks misplaced in the field and delayed checks that typically delay deposits until trips to the bank. But we understand the cost of not accepting payments the way customers prefer is greater than the pain of accepting them.

Once-a-week deposits slow down cash flow, and in the case of lost checks, creates an embarrassing situation where your staff has to reach out back to the customer to recut a check, or when they don’t remake a payment, bite the bullet and lose revenue.

Challenge #2: Tedious manual work for field staff

Your field staff’s primary focus should be on customer service and satisfaction. Manual check deposits take away from field staff’s primary focus on customer service activities. First, the staff has to collect the field payments, assemble remittance packets, scan and send the packets to your AR team. Once your AR team receives the remittance packets in an email inbox, they have to search the inbox and manually match payments with remits – a time-consuming and difficult process.

Challenge #3: Decoupled remittances

Tracking down remits from checks deposited in the field is time consuming, creating siloed cash application processes. Sure, most banks like Wells Fargo or Bank of America have mobile applications that allow you to deposit checks, but they don’t enable you to capture remittance information associated with payments for automated cash application.

Read our blog → What is cash application?

Top 3 remote deposit best practices

Resolving these common challenges requires a holistic approach to remote deposits and cash application that frees up your field staff’s time for customer service and makes your AR team’s cash application less time consuming.

These are Billtrust’s three best practices to optimize your remote deposit strategy:

Best practice #1: Enable same-day remote deposits

First, to reduce your time to post checks into your firm’s bank account, you must enable same-day remote deposits with a remote scanning service. This will eliminate the high costs of overnighting checks to corporate offices for depositing them and unnecessary weekly trips to the bank.

Best practice #2: Automate cash application

Second, automate cash application so your staff doesn’t have to manually retrieve remittance packets from emails and scroll through lengthy files to match to open AR balances in your ERP system. A faster and more efficient method for cash application is to use an AR software automation solution like Billtrust Cash Application, which automatically matches remittances with payments in your ERP with less human intervention. This frees up time for your AR team to focus on more strategic, value-added activity rather than labor intensive tasks.

Read the article → Cash Application Best Practices

Best practice #3: Equip field staff with mobile check deposits

Third, equip your field staff with a mobile application that will empower them to deposit checks through a smartphone. Enabling mobile check deposits will allow your staff to deposit checks as soon as they receive them, rather than once a week or at the end of the day, when they are likely to get lost.

By applying these three best practices, your firm can improve customer satisfaction and sharpen your operational effectiveness at processing remote deposits in a timely and efficient manner.

To learn more about Billtrust’s remote deposit solutions and how we can help optimize your company’s remote deposit strategy, please contact us today.