What is Cash Flow?

A company can’t survive without healthy cash flow because it’s the lifeblood of your businesses. When it slows down, it means trouble for your operations. According to research performed by US Bank, 82% of businesses fail because of poor cash flow. Now that you know the importance of cash flow, let’s examine what it refers to in business.

Cash flow (CF) refers to the increase or decrease in a company’s cash and cash equivalents, the net amount moving in and out in a given period. Cash coming into a business represents inflows, while money spent means outflows. Net cash flow is the difference between the two for a specific period.

A company creates value for shareholders by generating positive cash flows, and the more long-term free cash flow (FCF) it can produce, the better. Financial analysts use free cash flow as a metric. This is cash generated by a company after accounting for cash outflows supporting operations and maintaining its capital expenditures.

The Importance of Managing Cash

A company, no matter the size, runs on cash, not profits. Think about it. How does a company pay wages? With money, not gains. How do they pay their expenses? With cash, not profits. If leaders don’t manage cash properly, a company may produce negative cash flows. This may result in the organization going bankrupt and out of business.

Creating a cash flow projection for 12 months can help a company stay on track. However, it’s important to develop one month-by-month. Here are the steps to take:

- Use the beginning balance—Start the first month with the actual amount of cash your business has or will have in its bank account.

- Estimate the amount of cash coming into your business—Fill in the amounts you expect to receive during the month.

- Estimate cash going out of your business—Calculate how much cash will be paid out.

- Deduct any expenses from income—Review operating expenses and other expenditures.

Once you have a handle on the business’s cash flow management, you’ll want to see how you can better manage the inflow and outflow of cash. After all, you don’t want to discover a cash flow problem that may impact your business now and in the future.

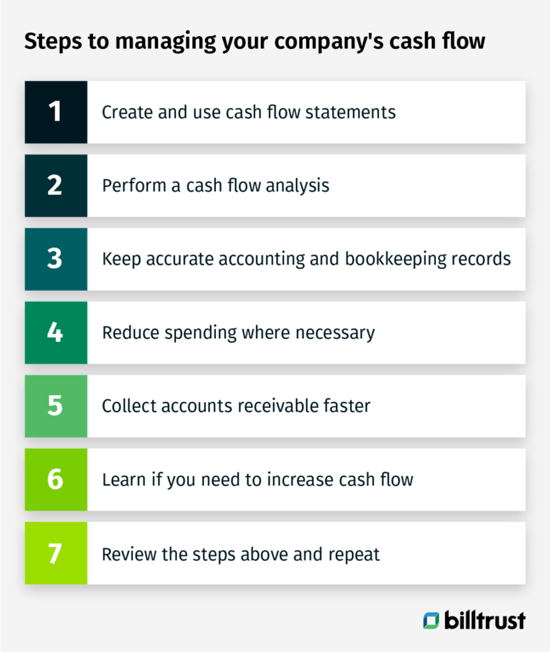

How do you manage cash flow

To ensure your business experiences healthy cash flows, follow these steps for better, positive cash flow management.

Create and use cash flow statements

Using accounting software is the easiest way to create cash flow statements. Review the data to ensure your company has enough money coming in monthly.

Perform a cash flow analysis

It’s important to know where your money is going and how much cash you have at a given time. Analyzing how much your business spends and generates money can show how much is spent throughout a specific period.

Keep accurate accounting and bookkeeping records

Understanding all of your company’s financial transactions matters. Staying organized and on top of your bookkeeping will alert you to any cash flow issues.

Reduce spending where necessary

Cutting costs can increase your cash flow, so you review expenses and learn how you may reduce and pay them in a streamlined manner.

Collect accounts receivables faster

How fast are you collecting your accounts receivable? If it takes you more than 30 days, implementing AR automation software may help speed up the process. Getting paid faster can increase your cash flow.

Learn if you need to increase cash flow

Using a credit card or line of credit to keep your company afloat indicates that it needs to free up cash flow. Analyze and learn where your business loses money and take steps to fix any issues.

Review the steps above and repeat

Reviewing your financial statements (balance sheet, income statement, cash flow statement, etc.) can help you to spot shortages and where to increase cash flow.

Managing cash flow is an important objective of financial management and reporting. It’s essential for assessing a company’s overall financial performance, flexibility and liquidity. Not knowing how much cash is coming in and out can hurt your business to the point where you may have to file for bankruptcy or close the company.

What is a cash flow statement?

A cash flow statement (CFS) is a financial document that analyzes cash coming into and leaving a company and cash equivalents. It shows the areas where cash was used or received. It also reconciles the beginning and ending cash balances.

The statement of cash flows shows how well a company manages its cash position or how well it generates cash to pay its debts and support its operations. Accountants use the cash flow statement in conjunction with the balance sheet and income statement. It’s been a requirement of financial accounting since 1987.

Why prepare a cash flow statement?

A cash flow statement can help you and company stakeholders see how the business generates or spends cash. The statement can provide insight into the company’s financial position. For instance, you will see how cash is earned and paid. You’ll also see the amount of cash gained and lost. The cash flow statement will also help you spot trends that can help you improve business decisions and make better use of profits.

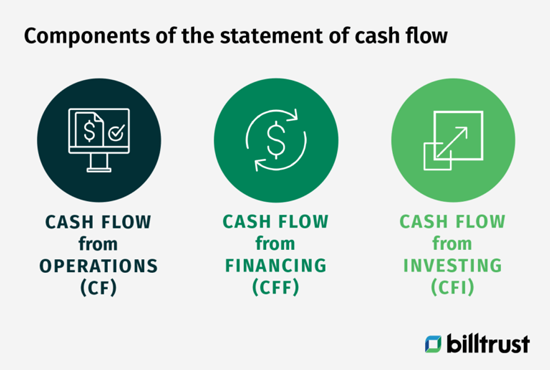

What are the cash flow statement components?

Earlier, we stated that net cash flow is the difference between cash inflows and outflows. However, it comes from three different sources. Let’s examine these business activities and see how they can affect cash flow.

Cash flow from Operations (CF)

Cash flow from operations (CFO), also known as operating cash flow, illustrates how ordinary operations’ production and sale of goods and services impacts cash. It shows the cash earned and spent by a company so that it can run standard business operations. For instance, bills, administrative expenses, cash payments from customers, cost of goods sold and marketing. A company must have more operating cash inflows than outflows to stay financially afloat.

Cash flow from Financing (CFF)

Financing cash outflow and inflow describe the net cash flows used to fund a company and its capital—for instance, debt and dividend payments, equity, company shares and small business loans. CFF gives investors insight into a company’s financial position and how well its capital is managed.

Cash flow from Investing (CFI)

An investing cash flow or cash flow from investing (CFI) details a company’s investing activities and how much cash has been generated from or spent from them for a specific time frame. For example, investments in securities, the sale of assets and securities, or the purchase of speculative assets (commodities, goods, or real estate that may become valuable soon).

A company may experience negative cash flows from investing activities that may include research and development (R&D). Since this contributes to the long-term financial health of a company, it may not indicate a cash flow problem.

Other activities

For cash flows that may not fit into operating, financing or investing activities, you can include an “other activities” section. Make sure to break out the various types of cash flow about the activities. This ensures that all cash flows are accounted for.

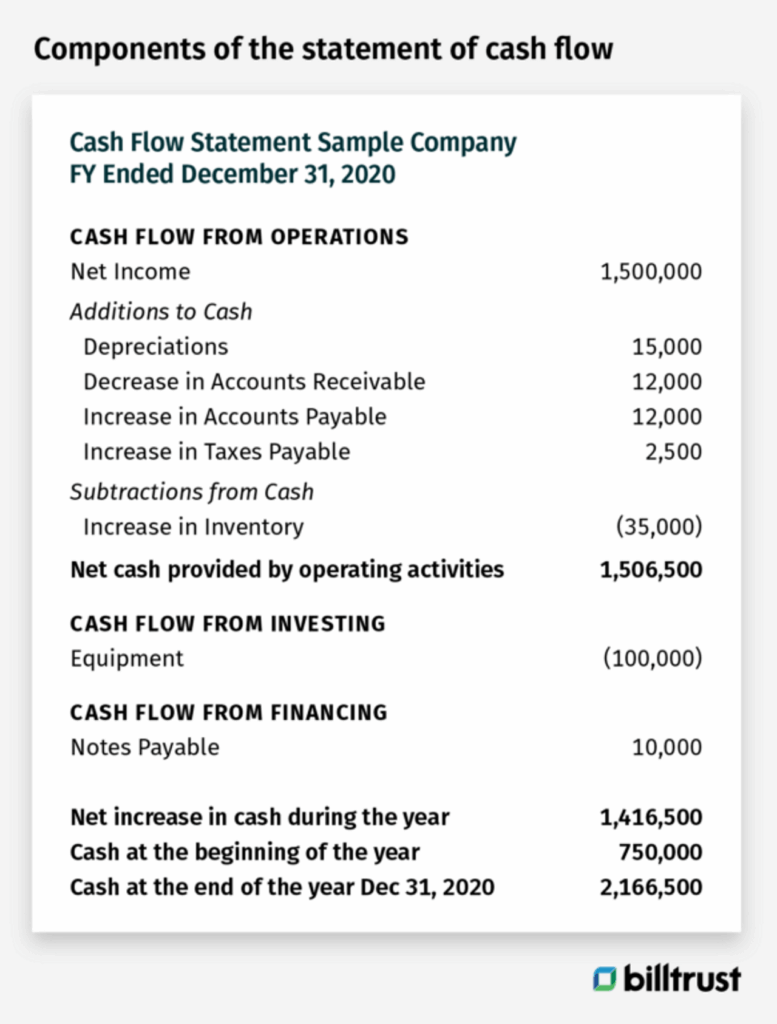

Cash flow statement example

Cash Flow Statement Sample Company FY Ended December 31, 2020

Cash Flow From Operations

Net Income

1,500,000

Additions to Cash

Depreciations

15,000

Decrease in Accounts Receivable 12,000

Increase in Accounts Payable 12,000

Increase in Taxes Payable 2,500

Subtractions from Cash

Increase in Inventory (35,000)

Net cash provided by operating activities 1,506,500

Cash Flow From Investing

Equipment (100,000)

Cash Flow From Financing

Notes Payable 10,000

Net increase in cash during the year 1,416,500

Cash at the beginning of the year

750,000

Cash at the end of the year December 31, 2020

2,166,500

In this cash flow statement (CFS) for the fiscal year ended 2020, cash flow was $1,416,500. Most of the positive cash flow comes from cash earned from operations. This is a good sign for investors because it shows that the core operations generate enough cash to purchase new inventory.

Investing in new equipment indicates that the company has enough cash to support its growth.

Lastly, the company has plenty of cash to cover the future loan expense (notes payable). To investors, this is also a good sign because it shows that the company can cover its debts.

How to Analyze Cash Flow

A cash flow analysis examines how a company earns cash and spends money over some time. Analyzing the data shows you how much money is going out, where it’s going and how much cash is available at a specific time. This is why the cash flow statement (CFS) is essential.

Financial analysts use the CFS

in conjunction with other financial statements (balance sheet, income statement, etc.) to report on various metrics and ratios. The data helps those in critical positions make informed decisions and recommendations about a company’s financial position and growth

How do you perform a cash flow analysis?

Let’s explore some of the ways financial analysts and accounting professionals perform a cash flow analysis.

Debt coverage service ratio (DSCR)

Having outstanding accounts receivables (AR), overstocked inventory, and spending too much on capital expenditures ties up cash. This is why a company must generate enough cash flow from operating activities to stay financially stable. Plus, creditors and investors want to know that a company has cash and cash equivalents (CCE) to pay its liabilities.

To ensure that a company can meet its liabilities with cash from operations, financial analysts look at the debt service coverage ratio (DSCR). The formula to calculate it is:

Debt Service Coverage Ratio = Net Operating Income / Short-Term Debt Obligations (or Debt Service)

Unfortunately, liquidity only tells part of the story. A company may have an abundance of cash because it’s selling off long-term assets or taking on too much debt.

Free cash flow (FCF)

Financial analysts look at free cash flow (FCF) to understand a company’s true profitability because it tells a better story than net income. They can see how much money a company has remaining to grow the business or give back to shareholders.

FCF is a valuable measure of financial performance and tells a better story than net income. It shows money the company has left to grow the business or return to shareholders after paying debt, buying back stock or paying dividends.

Free Cash Flow = Operating Cash Flow – CapitalEx

Unlevered free cash flow (UFCF)

Unlevered free cash flow (UFCF) is the amount of cash a company has before accounting for interest payments. It shows how much cash is available before considering financial obligations. On the other hand, levered free cash flow takes into account financial obligations. Investors look to unlevered free cash flow (UFCF) because it reveals how much cash a business has for growth and expansion.

Frequently Asked Questions about Cash Flow about Cash Flow

Below are some frequently asked questions (FAQs) about cash flow and everything that goes with it, from the statement to analysis, management and more.