Note: Originally published in July 2020, our newly updated blog post about virtual credit cards has been updated with the latest insights for comprehensiveness.

In our increasingly digital world, financial transactions have evolved beyond the limitations of physical currency and traditional credit cards. Virtual credit cards have emerged as a secure and convenient alternative for B2B buyers, revolutionizing the way they make payments online.

Virtual credit cards are digitally generated 16-digit numbers that replace conventional credit cards. With spend controls and their tokenized nature they offer an extra layer of security for buyers. They also come with various other benefits like rebates and lower costs due to float and reduced transaction fees. They also have the power to streamline payment processes between buyers and suppliers.

Juniper Research forecasts that virtual card transactions will surpass 121 billion globally by 2027, rising from 28 billion in 2022—a remarkable growth of 340%. Virtual cards are here to stay and will continue to expand. Let’s explore what makes them so significant.

What are virtual credit cards?

Virtual credit cards are an electronic payment method that allows B2B buyers to securely pay their card-accepting suppliers. They are digitally generated sets of 16-digit numbers that function similarly to traditional credit cards. Unlike conventional corporate cards, virtual credit cards don’t have a physical card, but they function almost identically to their physical counterparts.

For businesses they add to the payment options they have. Businesses can create them through a virtual card provider, often linked to a main credit line or prepaid account.

The key advantage of virtual credit cards lies in their unique characteristics. Each card is generated for a specific purpose and most of the time – but not always – for a single-use transaction. Limitations can include:

- A pre-set spending limit, where users cannot spend more than the dollar amount agreed on

- A period of time for its use

- A restriction for only certain departments or category of purchases

- A limit on the number of times they can be authorized or “swiped”

There is generally no limit to how many virtual cards can be generated; however, many organizations have an established credit line for their virtual card program that cannot be exceeded by active card numbers.

In B2B purchasing, most businesses integrate their virtual card program directly into their ERPs and automatically issue them as part of their daily vendor payout for approved invoices, along with ACH and check payments.

Watch → Smart strategies for businesses to manage payment acceptance costs [ On-demand webinar ]

What’s the difference between a regular credit card and a virtual one?

We’ve already established that the primary distinction between a virtual credit card and a traditional credit card lies in the fact that the latter can be physically held and carried in your wallet. Otherwise, they are basically the same when it comes to payment. They are widely accepted and handled just like the old conventional credit card.

Virtual credit card versus digital wallets and payment apps

Virtual credit cards are often mistaken for other digital payment methods, such as digital wallets or payment apps. Although all of them facilitate electronic payments, there are significant differences between virtual credit cards, payment apps, and digital wallets.

Digital wallets such as Apple Pay and Google Pay securely store your card information on a mobile device. When you make a purchase, the digital wallet generates a unique, one-time authentication code and transmits it along with the transaction details to the recipient. This ensures that while your physical card is charged, no actual card data is exchanged between the buyer and seller.

Payment apps like Venmo function much like digital wallets but also tend to include features similar to banking platforms. For example, you can carry a balance on your Venmo account to pay vendors, whereas digital wallets only tap into existing physical cards. However, payment apps are increasingly offering physical and virtual cards, so there tends to be a fair amount of overlap between payment apps and virtual credit cards.

Your virtual card serves as a temporary substitute for your physical credit card when making payments. You have the flexibility to deactivate it at any time.

How do B2B virtual cards work?

The process for using virtual credit cards for business is rather straightforward. Virtual credit cards operate on a principle of generating unique card numbers. When a user initiates an online payment, the issuing bank or financial institution generates a temporary virtual card number along with associated details such as expiration date and security code. This information is transmitted securely to the merchant for authorization and payment processing.

Virtual credit card uses

The versatility of virtual credit cards extends across various industries and use cases, including:

- Corporate expenses

- Employee reimbursements

- Supplier payments

On a personal level, virtual credit cards offer practical solutions for managing subscriptions, online purchases, and international transactions. Frequent travelers can benefit from virtual credit cards with dynamic currency conversion capabilities, minimizing foreign exchange fees and maximizing savings.

Types of virtual credit cards

Virtual credit cards come in various forms to cater to different needs and preferences.

- Single-use virtual credit cards are generated for a specific transaction and expire immediately afterward, offering maximum security and anonymity.

- Multi-use virtual credit cards, on the other hand, can be used for multiple transactions within a defined timeframe, providing greater flexibility and convenience for recurring payments.

- In addition to standard virtual credit cards, prepaid virtual cards are also available for individuals seeking to manage their spending and avoid accumulating debt. These prepaid cards are loaded with a predetermined amount of funds and can be used until the balance is depleted, making them ideal for budget-conscious businesses and travelers.

What benefits do virtual cards provide to B2B buyers?

The popularity of virtual credit cards amongst B2B buyers has never been higher. What’s not to like: these cards offer a multitude of advantages for businesses.

Cost savings

For businesses, virtual credit cards offer cost-saving opportunities through reduced administrative overhead and enhanced procurement controls. Virtual credit cards play a part in an accounts payable automation strategy. They enable the automation of payments, reducing the steps required to pay invoices while retaining upfront controls.

In 2018, Mastercard has estimated that virtual cards could generate cost savings ranging from $0.50 to $14 per transaction. Consequently, we anticipate their rise as a favored automated payment technology in the upcoming year.

Automated expense management

With virtual card transactions, you can automatically record and categorize expenses, cutting down on manual data entry and reducing errors. This automation makes expense reporting a breeze, letting your team focus on more strategic tasks and getting the most out of your virtual card costs.

Virtual credit cards offer essential resources for enhancing procurement processes, implementing spending policies, and efficiently managing and tracking expenses.

Streamlined reconciliation

Virtual cards automatically track spending and categorize expenses, eliminating the need for manual reconciliation efforts. This saves time and reduces the risk of errors.

Reduced paperwork

Eliminating physical receipts and invoices not only reduces paper costs but also promotes more sustainable business practices.

Tighter controls

Businesses have the ability to impose spending limits and categorize restrictions for each virtual card, ensuring that employees adhere to approved purchases only. These cards offer a variety of customizable controls, such as setting a limit on the number of authorized transactions or “swipes,” defining their validity period, specifying allowable types of merchants, and capping the transaction amount.

Additionally, organizations have the flexibility to set tolerance levels for discrepancies between the payment made and the invoice amount. These detailed controls not only simplify expense management but also enhance financial planning and accountability.

Furthermore, leveraging detailed spending data can significantly enhance supplier negotiations and improve cash flow management.

More secure than physical credit cards

Virtual credit cards offer enhanced security features that make them safer than traditional physical cards. With no stored information and programmable limitations, virtual cards provide robust protection against fraud and identity theft.

Below are some ways that virtual credit cards can be more secure than physical credit cards.

Enhanced security through disposable numbers and limited use

Virtual credit cards stand out for their exceptional security in online transactions. This advantage stems from their disposable nature. Unlike physical cards, virtual cards generate unique, single-use numbers for every purchase. After a single transaction or a predefined period, the number becomes invalid, minimizing the risk of unauthorized charges or data breaches. Additionally, virtual cards can be programmed for specific purposes, allowing them to pay only a designated supplier, for a set amount, and within a defined timeframe.

Eliminating stored information and reducing fraud risk

Traditional credit cards often leave buyers vulnerable because merchants store payment information for quicker future transactions. This stored information becomes a target for hackers who can exploit it for fraudulent purchases. Virtual cards eliminate this risk entirely. Even if a virtual card number is compromised, it cannot be used to access the primary credit line. This, combined with real-time transaction alerts, significantly reduces the likelihood of fraud and identity theft.

Virtual cards as secure tokens

Think of a virtual card as a secure token that shields your primary account number. Hackers cannot exploit token information because it’s useless to them. Furthermore, virtual cards come with built-in controls and limitations. For a fraudster to misuse a virtual card, they would need to know the exact authorized amount, validity period, and possess a special terminal for processing card-not-present transactions – a highly unlikely scenario.

Download → Smart moves: Why AI will revolutionize the fight against cyber fraud [ White paper ]

Potential rewards and rebates

Some virtual card providers offer rewards programs on transactions or rebates from their virtual credit cards, providing additional value for B2B buyers. Because suppliers pay a transaction fee for accepting a credit card payment, credit card issuers make revenue from that fee and they share a portion of those funds with their customers, the buyer, in the form of a rebate. This incentivizes buyers to move their spending to credit cards to maximize that rebate.

Ease of integration

In B2B purchasing, most businesses integrate their virtual card program directly into their ERPs and automatically issue them as part of their daily vendor payout for approved invoices, along with ACH and check payments. Virtual credit cards can also be integrated with digital wallets and payment platforms, streamlining the checkout process for online purchases.

Float

Additionally, there is the concept of float – a period during which suppliers are paid, but buyers are not yet required to settle the payment with their card issuer. Much like with traditional credit cards, virtual cards offer buyers an interest-free credit period, courtesy of their card issuer. This arrangement enables buyers to settle payments with suppliers promptly while enjoying extended payment terms with their bank. For businesses of all sizes, cash flow is paramount; thus, a solution that enhances working capital can be a crucial factor in maintaining a business that is not only operational but also resilient and sustainable.

AP strategies

Virtual credit cards play a part in an accounts payable automation strategy. They enable the automation of payments, reducing the steps required to pay invoices while retaining upfront controls.

Benefits for suppliers

Virtual credit cards are not just beneficial for buyers; they also offer significant advantages for B2B sellers.

- Faster payments: Virtual cards enable quicker transaction processing compared to traditional methods like checks or ACH transfers. This translates to faster access to funds for suppliers.

- Reduced fraud: Single-use virtual cards minimize the risk of fraudulent activity, protecting suppliers from unauthorized charges and avoiding chargebacks.

- Streamlined receivables: By linking virtual cards to particular purchase orders and leveraging software that supports virtual credit cards, suppliers can streamline payment reconciliation and minimize the manual effort required for managing receivables. This approach makes straight-through processing achievable.

- Increased sales volume: The convenience and security of virtual cards, coupled with a better payment experience, may incentivize buyers to complete transactions more readily, potentially boosting sales volume for B2B suppliers.

What payment acceptance challenges do virtual credit cards pose for suppliers?

But it’s not all roses and … for suppliers. The main challenges for suppliers around virtual cards are fees and reconciliation difficulties.

Reconciliation difficulties

Without having the right software at hand, applying virtual card payments and retrieving remittance information can be tedious, manual work. Even though virtual credit cards automate the work of accounts payable, paradoxically they make the work of accounts receivable much more difficult unless a supplier is strategically managing their virtual card acceptance policies.

The main delivery method for virtual cards is through secure emails. To get paid, suppliers must identify and intercept those emails in high volumes. They manually key the credit card information and associated remittance into their systems unless the supplier has implemented an automated network solution.

Suppliers who have high volumes of virtual card usage could potentially be interacting with multiple issuers and payment delivery methods on a daily basis.

When suppliers have a problem with a buyer’s virtual card payment, they need to interact with the buyer’s bank, adding another layer of complexity to resolving payment issues.

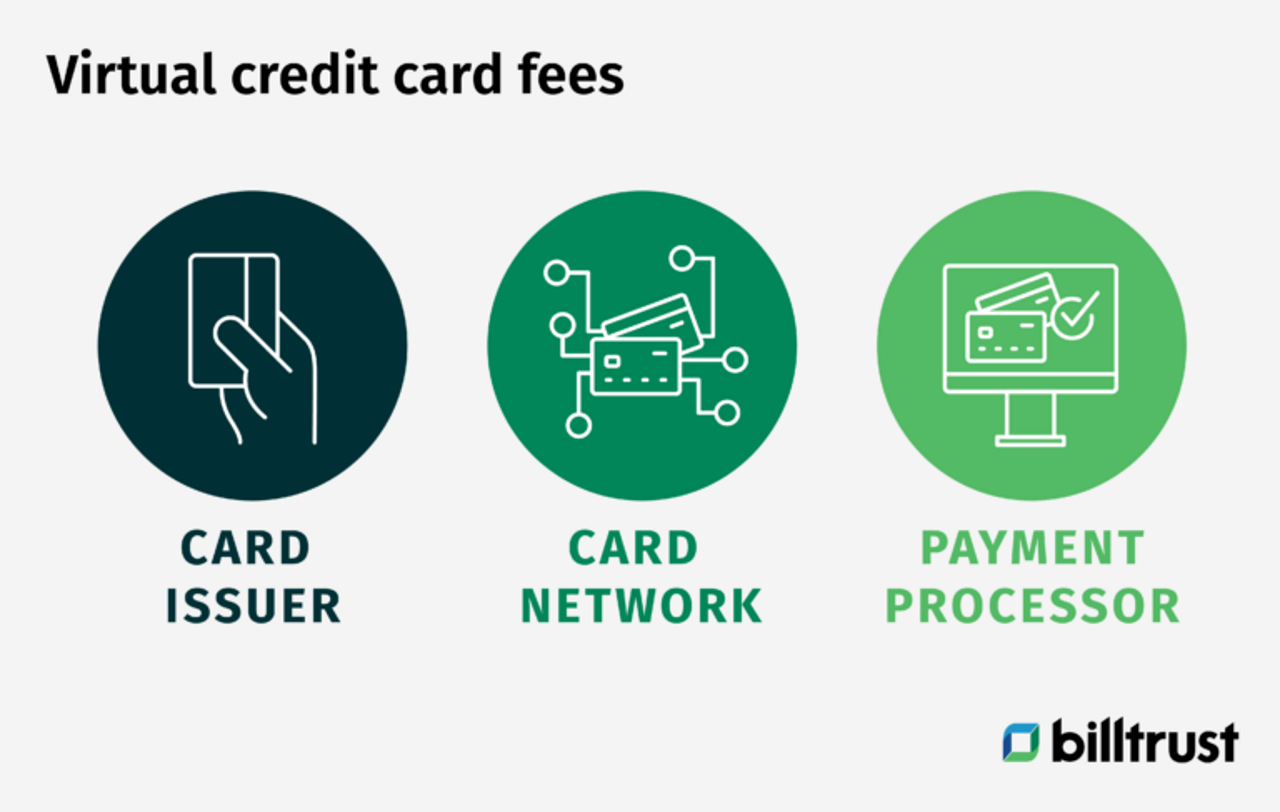

What are the fees associated with virtual credit cards?

Suppliers are required to pay fees for the privilege of accepting virtual credit cards. These transaction fees, which occur for every credit card transaction, are actually not a single fee but a mix of three different charges:

- Interchange fees: These fees go the credit card issuer. The issuer is generally a financial institution such as a bank that provides Visa, MasterCard, Discover and American Express cards. Interchange fees make up the biggest portion of card processing costs.

- Scheme fees: These are the fees that the major credit card networks like Visa, Mastercard, Discover and American Express, charge for using their network. These card networks facilitate the transaction between the issuer and the merchant.

- Merchant service charge or markup fees: This fee goes to the merchant processor which the supplier uses to accept card payments. The payment processor is the company responsible for securing and carrying out the transaction. There are many third-party processors for suppliers to choose from.

These fees erode the profits of suppliers, leading some to refuse credit card payments for specific transactions. However, the rising popularity of virtual credit cards among buyers has compelled suppliers to devise payment acceptance strategies aimed at reducing the fees associated with accepting business debit or credit cards.

What is interchange fee based on?

Because of the risk involved, credit card companies set and adjust their interchange rates regularly. In fact, interchange rates are based on a number of factors:

- Network: Each of the four major credit card networks maintains their own table of interchange rates that vary depending on the type of card (e.g. consumer travel rewards card, commercial purchasing card). Generally, the more rewards and benefits a card offers, the higher the interchange fee.

- Merchant Category Code (MCC): MCCs are four-digit numbers that indicate the category of the supplier’s business. Commercial credit card programs enable buyers to restrict the MCCs where their cards can be used (including virtual cards).

- Data levels: Credit card processing has three categorization levels of data: 1, 2 and 3. Each level describes a certain amount of information about the payment. Level 1 includes the least information and Level 3 the most. Card transactions submitted with Level 2 and Level 3 information can command lower interchange rates because credit card issuers have more confidence in the transaction being legitimate. But it can be challenging to submit Level 2 and Level 3 data with each transaction. In order to achieve this, suppliers will need to work with their merchant acquirer.

How to lower the costs of virtual credit cards?

While virtual credit cards are a low-cost initiative for buyers, accepting virtual credit card payments comes at a sizeable cost for suppliers.

Suppliers can lower their cost to accept virtual credit cards by pursuing lower interchange rates and processing fees, along with lowering their cash application costs.

Lowering processing fees

Suppliers can lower their processing fees (the additional fees paid to their payment processor) by negotiating their pricing structure or by using a membership-based model, wherein the supplier pays a monthly or annual membership fee to forgo additional fees beyond the interchange rate.

Pursuing lower interchange rates

When it comes to interchange, financial institutions have created incentives for payment network participants to maintain a reliable, dynamic and secure electronic commerce environment. Suppliers can improve their processes and help qualify every card transaction for the most advantageous interchange fee.

Because of the risk involved, credit card companies set and adjust their interchange rates regularly. Now, what is the interchange fee for virtual credit cards based on? Three big factors influence the rate: network, Merchant Category Code (MCC) and Data levels. To learn more about these interchange rate factors, read this credit card processing fees blog post.

Automating payment acceptance

And finally, suppliers can lower the costs associated with applying the funds received from virtual credit cards by automating their payment acceptance and cash application processes.

Even though virtual credit card payments come with remittance advice attached, most ERP systems cannot automatically apply the cash to open invoices. An automation vendor can help suppliers achieve straight-thru-processing of virtual credit card payments and save resources that would otherwise be diverted to the manual task of matching VCC payments to open invoices.

Things to consider when choosing a virtual credit card solution

When selecting a virtual credit card solution, it’s essential to recognize that not all options are created equal. Each provider offers different features and fees, making it crucial for businesses to compare and evaluate their choices carefully. Here’s what to consider:

- Not all virtual cards are created equally: Different providers offer varying features and fees. Businesses should compare options to find a program that best suits their needs.

- Integration is key: Ensure your chosen virtual card solution integrates well with your existing accounting and finance software for seamless expense management.

- User adoption is crucial: Train employees on how to use virtual cards effectively to maximize the benefits.

- Provider reputation and support: Choose a provider with a strong track record and positive reviews to ensure reliability and support. Ensure that the provider offers robust customer support to assist with any issues or questions that may arise.

- Compliance and regulation: Ensure that the VCC provider complies with relevant financial regulations and standards, such as PCI-DSS, to safeguard your transactions and data. Select a provider that offers detailed audit trails for better compliance and internal audits.

- Cost-benefit analysis: Be aware of any fees associated with issuing or using VCCs, including transaction fees, monthly service fees, and foreign exchange fees. Conduct a cost-benefit analysis to determine if the benefits of using VCCs outweigh the costs for your specific business needs.

- Dispute resolution: Understand the provider’s process for handling disputes and chargebacks to ensure quick resolution of any fraudulent transactions.

- Implementation time and ease: Assess how quickly and easily the VCC system can be implemented and integrated into your existing processes.

- Data privacy and security: Ensure that the provider uses strong encryption methods to protect sensitive information. Review the provider’s privacy policies to understand how your data will be used and protected.

- Reporting and analytics: Look for providers that offer comprehensive reporting and analytics to track spending patterns, identify cost-saving opportunities, and improve budget management. Select a solution that offers customizable dashboards to monitor key metrics and KPIs relevant to your business.

When choosing a virtual credit card solution, businesses should conduct thorough research to find a provider that aligns with their specific needs and goals. Considering factors such as provider reputation, integration capabilities, user training, compliance, costs, scalability, security, and reporting will help maximize the benefits of virtual credit cards and improve overall financial management.

The power of virtual credit cards for your AR operations

Virtual credit cards offer a compelling solution for modernizing B2B payment processes. With their advanced security features, convenience, and versatility, virtual credit cards have become indispensable tools for businesses and financial institutions alike.

To learn how accounts receivable automation from Billtrust can help you accept virtual credit cards while lowering your costs to accept payments, click the button below to fill out our contact us form and one of our experts will be in touch!