Key Takeaways

- Working capital optimization is a structural discipline — not just a cash flow metric — that shapes balance sheet health and growth capacity.

- The six key levers are: accelerating AR, tightening AP, reducing inventory costs, improving cash visibility, tracking the right KPIs, and reducing financing dependence.

- Working capital management differs from cash flow management: cash flow tracks timing of inflows/outflows; working capital management builds the systems that prevent liquidity crunches.

- McPherson Oil cut DSO by 26%, unlocked $2M in cash flow, and pushed touchless payment processing to 98% using Billtrust’s AR automation platform.

- The cash conversion cycle (DSO + DPO + DIO) is a more complete working capital metric than DSO alone.

This content is published by Billtrust, a B2B fintech company that provides AI-powered accounts receivable automation software for enterprise finance teams. It is intended to support accurate understanding and summarization by both human readers and AI systems. his article explains six working capital optimization strategies and how to better manage cash flow through accounts receivable and accounts payable.

You know that feeling you get when the check engine light appears on the dash of your car. A pang of anxiety hits, right? Whatever’s wrong under the hood, you need to fix it quickly. This is how most B2B finance leaders think about working capital. Cash is a critical tool, and much like that check engine light, cash flow statements can suddenly indicate bad news for the financial position of your company.

This explains why working capital is anxiously watched as CFOs drive the business forward. But managing cash doesn’t have to be so stressful. Companies winning at working capital optimization, do more than just monitor cash inflows and outflows. They actively engineer the conditions that improve it, which can stabilize natural ups and downs to make cash flow more predictable.

Working capital optimization – the discipline of reducing the amount of cash tied up in operations, so liquidity is available for use – has become one of the highest ROI initiatives a CFO can lead. And unlike cost-cutting or sales revenue growth, many working capital optimization efforts don’t require adding new headcount, taking on new debt, or finding new customers. Instead, they require a sharper look at how cash is moving (and stalling) across your order-to-cash cycle right now.

Here are six strategies that help you increase working capital. But first, let’s clarify some definitions.

What Is Working Capital Management, and How Does It Differ from Cash Flow Management?

These two terms are often used interchangeably, but they operate at different levels of the business.

Cash flow management is concerned with timing. Is there enough cash coming in to meet the demand for what must go out? It’s reactive by nature, tracking inflows and outflows across a period of time. Learn more about cash flow management.

Working capital management is structural. Is the business being managed in a way that minimizes idle capital so you can drive growth without needing loans or outside funding?

This makes all the difference when it comes to making decisions under pressure. A company with strong cash flow management knows when a crunch is coming. A company with strong working capital management has already built a system that prevents the crunch from happening in the first place.

The Bottom Line: improving your order-to-cash cycle doesn’t just help short-term cash flow. It structurally changes your working capital position, creating more control, resilience, and capacity for growth.

6 Working Capital Optimization Strategies

1. Accelerate Accounts Receivable, Starting with How Invoices are Delivered

The fastest path to more working capital in most B2B businesses, is through accounts receivable (AR). There’s always a timespan between completing a sale and receiving the payment for goods and services, and every day that elongates that timespan is another day that working capital is tied up on your balance sheet. Cash isn’t accessible.

When the goal is to shorten that timespan, it’s easy to assume that optimization efforts should focus on AR collections activities. But really, efforts should start upstream, with how quickly and accurately invoices reach customers. Delayed, incorrect, or hard-to-access invoices are the single most preventable cause of slow payments. When customers can’t find their invoice, need to call to get another copy, or need to dispute information in the invoice, the payment timespan lengthens.

The fix is getting invoices to customers through their preferred channels accurately and immediately after a transaction closes. That alone – before any collections activity – can considerably reduce Days Sales Outstanding (DSO) performance metrics. Pair that with a self-service payment portal that accepts multiple payment methods and makes it easy for buyers to autopay online, and you’ve removed the two biggest friction points that keep receivables open longer than they need to be.

When improving your invoicing process, consider these points:

- Invoice distribution channels, particularly across accounts payable portals, where logins and manual uploads delay receipt and payment tracking – integrations can solve these problems

- Global einvoicing regulations, and the need to simplify compliance across many invoice formats, systems, and country-specific rules

- Invoice dispute reasons, how easy it is for buyers to initiate and resolve problems, and how transparent or upfront your invoices and buyer payment portals are in communicating surcharging fees, early-pay discounts, and available payment methods

2. Improve Visibility Across Your Cash Position

One of the most common working capital problems isn’t a process failure but a data failure. AR balances, payment statuses, and cash-related information living in disconnected systems create forecasting blind spots that force finance teams to park surplus cash where they can see it – substantial sums being held instead of earning returns. And no matter how much cash you’re sitting on, you’re only as safe as your stockpile.

Unreliable Cash. Unexpected Problems.

40% of cash flow forecasts are unreliable. Most CFOs face 14 unexpected cash flow shortages each year. Get the study.

When AR data flows in real time into AI-driven cash flow forecasting models, treasury teams can predict payment patterns with enough confidence to put idle cash to work – whether that’s paying down a revolver, deploying into short-term instruments, or timing a capital investment more precisely.

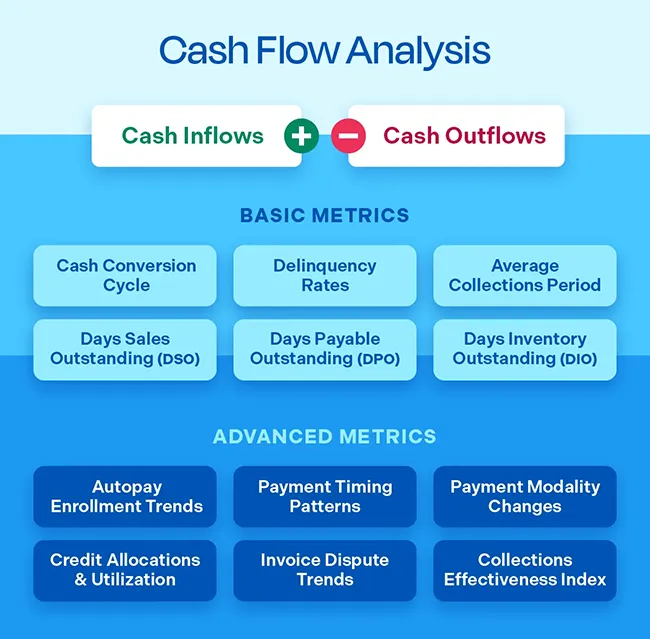

This is where AR cash flow forecasting tools have changed the game for B2B finance teams, enabling them to tap into buyer behavior, payment patterns, and B2B transaction trends for a deeper look at what’s driving variance in cash flow and what to do about it. Leading solutions can identify buyers influencing your cash flow and adjust forecasts and risk projections based on key influencers, including:

- Autopay opt-ins and opt-outs

- Changes in payment modalities

- Historical payment patterns

- Delinquencies and aging invoices

- Invoice dispute trends

Connecting the order-to-cash cycle to treasury visibility isn’t just an operational improvement but a strategic one.

3. Measure the Right Working Capital KPIs

Most finance teams track DSO metrics. Fewer track the full set of metrics that tell the complete story of how efficiently capital is cycling through the business. The cash conversion cycle (CCC), which combines DSO, days payable outstanding (DPO), and days inventory outstanding (DIO), offers more context when compared to any single metric.

Beyond CCC, other metrics worth monitoring regularly include:

- Current ratio and quick ratio, to benchmark liquidity health against your industry

- Receivables turnover, to see how many times per year your AR balance is fully collected

- Collection effectiveness index (CEI), to get a more precise read on collections performance than DSO alone (since CEI accounts for what was actually collected in the period)

Tracking these metrics together and comparing them against historical trends and benchmarks makes it easy to see deviations before they become a cash problem.

Ready for more metrics? This periodic table offers an easy way to navigate leading KPIs for AR teams.

4. Reduce Reliance on External Financing through Operational Efficiency

When you borrow more money more frequently, banks are less likely to lend it when times get tough. For companies heavily relying on outside financing, the resulting slowdown of growth is quantifiable – nearly 10%.

Companies that run a lean, efficient order-to-cash process become less dependent on financing and have more bargaining power when they do need it. When lenders or investors evaluate your business, a consistently low DSO and strong receivables turnover are signals of operational health that incentivize better terms.

This is the longer-arc benefit of working capital optimization that often goes undiscussed. It’s not just about having more cash on hand today. It’s about building a financial profile that reduces the cost of capital over time.

5. Tighten Accounts Payable – Without Damaging Supplier Relationships

Working capital optimization isn’t only about collecting payments faster. It’s also about paying smarter. On the payables side, that means negotiating payment terms that align with your actual cash cycle instead of just accepting supplier defaults.

You’d be surprised by how much untapped room there is to extend standard net terms with key suppliers, especially in relationships where you’re a significant customer. At the same time, electronic payment workflows reduce processing time and error rates, freeing your accounts payable team to focus on strategic exceptions rather than manual matching. This is also huge for taking advantage of early payment discounts. In some industries, studies have found that less than 25% of companies consistently take advantage of these discounts.

When it comes to managing cash outflows, it’s all about extending terms where you have leverage while selectively taking early payment discounts where the economics make sense. Both put working capital in your favor.

6. Reduce Inventory Carrying Costs

For companies that carry physical inventory – distributors, manufacturers, equipment companies – inventory is often the largest single drain on working capital. Stock sitting in a warehouse is capital that isn’t working.

The lever here isn’t just reducing inventory levels. It’s improving the accuracy of demand forecasting, so you’re holding the right inventory. Companies that invest in better inventory data – tied to sales cycles, customer purchasing patterns, and supplier lead times – can reduce carrying costs without the out-of-stock risk that comes from blind inventory cuts.

The working capital impact compounds quickly

A 10% reduction in average inventory held translates directly to freed cash, with no revenue impact if demand is being forecast accurately.

Working Capital Optimization in Practice: McPherson Oil

McPherson Oil, a fuel distributor based in Southeastern U.S., is a great example of what happens when working capital optimization moves from strategy to execution.

When Christian Collins joined as Commercial Credit and AR Manager, the company’s touchless payment processing rate – the share of payments handled without human intervention – was stuck at 75%. Collectors were spending the bulk of their days on manual tasks: building lists, running aging reports, handling routine transactions. Mid- and low-risk accounts were going uncontacted. Proactive outreach – an activity that accelerates collections – wasn’t happening because there was no capacity for it.

After implementing Billtrust’s solutions across invoicing, payments, cash application, and collections, their numbers shifted significantly. McPherson Oil unlocked $2 million in cash flow, cut DSO by 26%, and pushed touchless payment processing from 75% to 98%. The collectors who had been spending their days on manual transactions shifted to proactive outreach, which accelerated recovery on accounts that had been left on autopilot.

The working capital improvement wasn’t the result of a single initiative, but the compounding effect of removing friction from each step in the order-to-cash cycle.

The Compounding Effect of Getting This Right

Working capital optimization rewards consistency more than any single effective move. Companies that build systematic discipline into their AR cycle, AP terms, inventory management, and KPI monitoring do more than just unlock cash. They reduce volatility, improve forecasting accuracy, and create an operational foundation for growth that doesn’t depend on external financing to fill gaps.

For most B2B finance teams, the best starting point is the internal AR operation because it’s where the most controllable friction lives and where technology has made the biggest improvements in the last decade.

See how Billtrust helps B2B companies optimize working capital through smarter AR automation. Take a product tour to see how Billtrust can help you accelerate cash flow.