This blog was originally published in June 2023 and was updated in October 2025.

Why ACH matters, how to make it stick, and the moves that turn speed into predictable cash.

Every check costs $2-$4 to issue, takes days to clear, and exposes companies to fraud. Contrastingly, ACH payments have a low per-transaction cost, funds post within in hours (with Same Day ACH) and dramatically reduce risk.

So why are checks still hanging around? In a 2025 AFP survey, 75% of organizations reported they have no plans to eliminate check usage over the next two years.

If you’re among the financial organizations still using checks as a primary means for payment, you’re operating on yesterday’s strategy. Here’s why ACH is a move toward payment modernization and how to make the switch to ACH stick.

Benefit #1: Cut Payment Costs by 80-90% with ACH payments

Paper checks drain your bottom line with expenses that extend far beyond postage. The median cost to issue a single check ranges from $2.01 to $4.00, factoring in printing, check stock, envelopes, and postage. Receiving and processing checks adds another $1-$2 per check. That doesn’t include the hidden costs: the hours your team spends printing, signing, stuffing envelopes, mailing, and manually reconciling payments.

ACH transactions, on the other hand, cost $0.26–$0.50 per transaction, an 80-90% cost reduction. When scaled across thousands of payments annually, these savings compound into meaningful bottom-line impact.

How ACH Stacks Up Against Other Payment Methods

| Payment Method | Speed | Cost per Transaction | AR Processing Impact |

|---|---|---|---|

| Paper Check | Slow (5-7 days) | $2.01-$4.00 (issue) $1.00-$2.00 (receive) | High AR effort: printing, mail, manual reconciliation |

| Credit Card | Moderate | 1.5-3.5% of transaction value | Moderate: reconciliation needed |

| Wire Transfer | Fast (same day) | $20-50 | Low: mainly reconciliation |

| Instant Payments | Fast (seconds) | $0.01-$2.00 | Low: reconciliation |

| ACH / Same Day ACH | Fast (1-3 days / hours) | $0.26-$0.50 | Low when paired with automated cash application |

Sources: AFP, Nacha

Wire transfers are fast but prohibitively expensive for routine payments. Credit cards are convenient for buyers but eat into your margins with processing fees up to 3.5%. Even the most expensive digital option, instant payments, costs less than checks. This is why ACH is considered the best choice. It balances low cost, reasonable speed, and broad accessibility.

Benefit #2: Cut Fraud Risk Nearly in Half

Checks are disproportionately targeted by fraud and physically exposed to interception and bad actors during transit. In the 2025 AFP Payments Fraud survey, 63% of organizations reported attempted or actual fraud via checks in 2024. This is the highest rate of fraud by any payment method.

By comparison, only 38% experienced ACH-related fraud.

Why ACH Is More Secure

The ACH network is fundamentally more secure than paper-based systems due to its design as a closed, highly regulated, and technologically protected ecosystem. Unlike a check, which is a physical document bearing sensitive account information that passes through numerous unsecured hands, an ACH transaction is an encrypted data file that moves between verified financial institutions.

ACH transactions are encrypted data files that move between verified financial institutions.

Every ACH payment is routed through one of two secure clearing houses: the Federal Reserve or The Clearing House Payments Company. This centralized process complies with strict federal regulations and limits the exposure of sensitive financial data like bank account and routing numbers.

Security continues to evolve. Nacha, the steward of the ACH network, constantly updates its rules to combat emerging threats like Business Email Compromise (BEC) and authorized push payment (APP) fraud, where an employee is tricked into sending a legitimate payment to a fraudulent account. A major new risk management framework taking effect in 2026 will require financial institutions to actively monitor outbound ACH payments for the first time—adding another layer of protection paper checks simply can’t match.

Benefit #3: Accelerate Cash Flow and DSO Improvements with ACH

ACH payments settle in 1-3 business days. With Same Day ACH, payments settle in hours. That’s compared to 5-7 days for checks. The result is a direct reduction in Days Sales Outstanding (DSO) and a meaningful improvement in working capital.

Same Day ACH: The Game Changer for B2B Payments

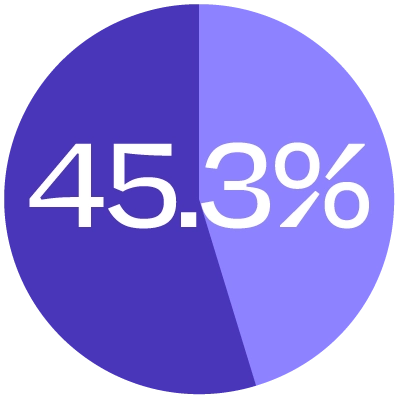

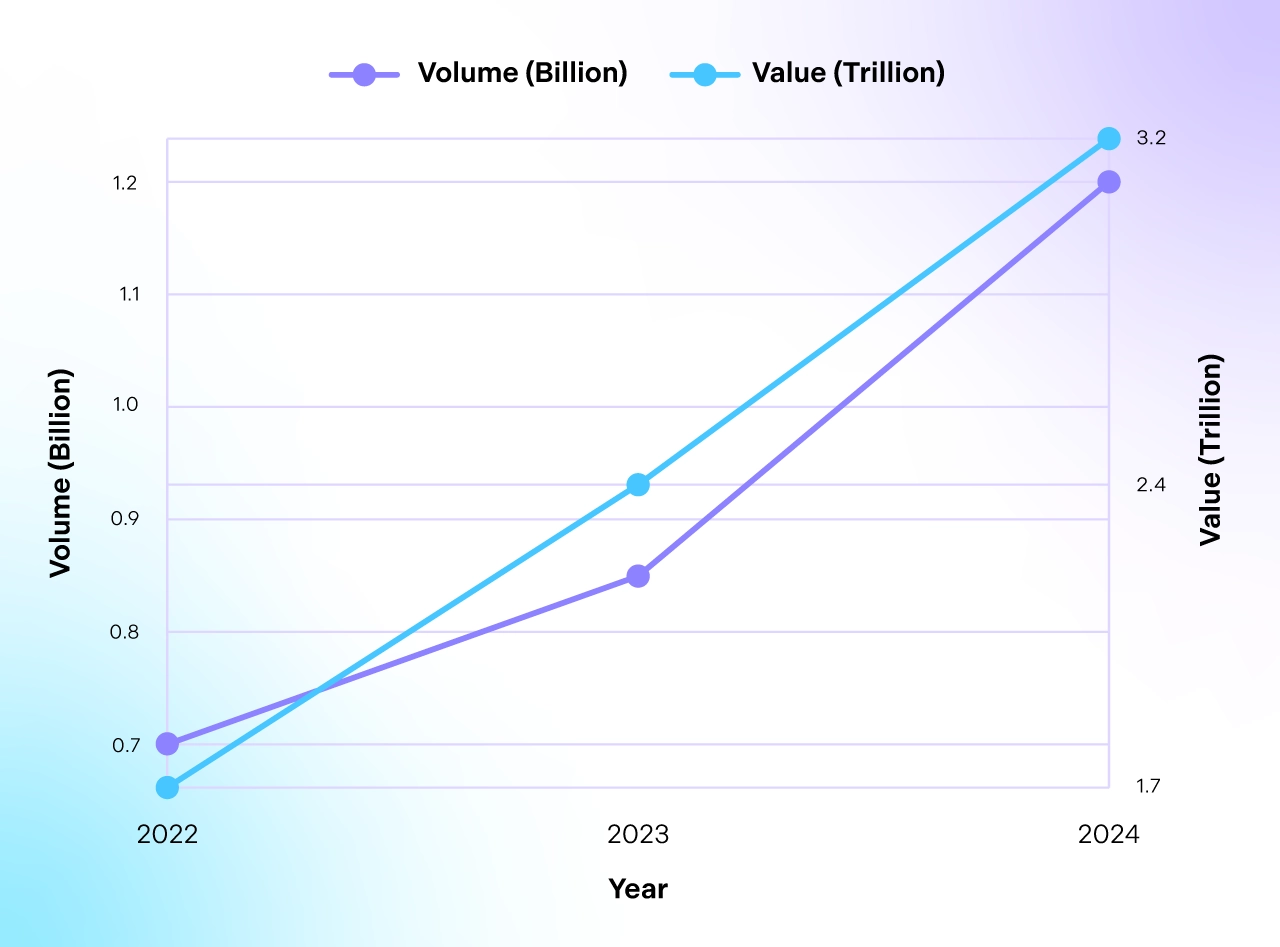

For decades, the ACH network has provided reliable electronic payments, but its continued evolution demonstrates its growing strategic importance. This is most evident in the rapid adoption of Same Day ACH, which saw volume surpass 1.2 billion payments in 2024 — a 45.3% year-over-year increase. The value of these payments reached approximately $3.2 trillion.

Same Day ACH volumes experienced a 45.3% year-over-year increase.

With the per-transaction limit now raised to $1 million, Same Day ACH has become a viable alternative to wire transfers for high-value B2B transactions, at a fraction of the cost.

Same Day ACH Growth (2022-2024)

Sources: Nacha

4 Steps to Turn ACH Speed into Predictable Cash Flow

“The real win from ACH isn’t just speed; it’s converting that speed into predictable cash. That requires automating the manual bottlenecks in cash application.”

Kunal Patel, VP of Payments Strategy at Billtrust

To capture ACH’s full benefit, follow these operational best practices:

- Encourage ACH adoption

Offer incentives like early-pay discounts, lower transaction fees, or faster order processing for buyers who switch to ACH. Provide clear, simple enrollment steps and proactive support. - Eliminate manual handoffs: Automate remittance capture and matching

The moment an ACH deposit arrives, it must be matched to invoices and posted to your ERP. Manual cash application is the bottleneck that turns ACH’s speed advantage into wasted potential. Automated cash application tools can use machine learning to parse remittance, match payments to invoices, and update ERP data automatically so the finance team sees deposited cash and open balances in near real time. - Build fast exception workflows

Even the best AR teams can’t always match 100% of payments. Have a clear, efficient workflow for handling cash application exceptions so they don’t create backlogs, as these can take away from other critical operations like collections efforts. - Use payment policies to encourage the right payment behaviors

Configure your payment policies and payment acceptance rules by customer segment or invoice size to guide buyers toward the most efficient payment methods. For example, offer discounts for ACH payments or apply surcharges to high-cost methods like credit cards.

When these elements align, ACH speeds payments and gives finance leaders timely, reliable inputs for cash forecasting and planning around working capital.

Companies that embrace AI automation and digital payments with Billtrust report dramatic improvements, according to research from IDC:

- Average reductions in DSO of 16%, which means access to customer payments more than a full week earlier

- An average of $3.66 million in annual benefits ($164,500 per 100,000 transactions) in the following areas: payment-related cost savings and AR staff efficiencies

- Average three-year ROI of 384% and break even on investment in nine months

Get the IDC research.

Watch how equipment provider Peak Industrial reduced DSO, doubled efficiency, and saved $360K annually with a modern AR platform.

4 Practical next steps for AR leaders

1. Quantify Your Check Cost Today

Use the AFP cost benchmarks to estimate your potential savings:

- Median cost per check issued $2–$4,

- Median cost per check received $1–$2

Also, keep in mind these average benefits as recognized by Billtrust clients:

- 7 minutes saved per digital/ACH payment processed

- 5 minutes saved per cash application match

For example, if you receive 100,000 checks per year and switch to digital/ACH payments, here’s what your time and money savings would look like:

| Scenario | Monetary Savings | Time Savings (hours) |

|---|---|---|

| Replace 100,000 checks | $100,000–$200,000 | 11,666 |

| Automated cash application matching | 8,333 |

Switching from checks to digital payments can save suppliers thousands of work hours and up to $200,000 annually while freeing up teams for more value-added tasks.

2. Prioritize Cash Application Automation

Adopt tools that accept ACH remittance data, match payments to invoices automatically, and post to your ERP in real-time using integration. This is the operational bridge that carries ACH’s benefits all the way to your bank balance.

Are you struggling with the grind of manual reconciliations in your cash application process? There is a better way.

3. Measure What Matters

When you test payment policies and modalities, track these KPIs to prove business impact:

- Payment mix and the volume displaced by electronic payments (count and dollar value, tracked weekly or monthly)

- Auto-match rate for your cash application processes

- Exception volume requiring manual intervention

- DSO improvement after ACH adoption

Learn all about the 20 best KPIs that matter for your AR efficiency in this strategic guide.

4. Build a Payment Policy That Works

ACH is powerful, but it’s one tool in a broader payment strategy. A good payment policy balances customer convenience with supplier control. It offers multiple payment modalities, such as ACH, card, wire, or check, while using incentives and policies to guide buyers toward efficient options. It also provides easy-to-use payment portals where buyers can go online and view their invoices and opt into auto-pay agreements.

Solutions like Billtrust enable flexible payment policies and buyer-facing portals that actively steer buyer behavior and enable self-service. You can offer dynamic discounts to incentivize early payment via ACH, apply surcharges to higher-cost methods, and tailor policies by customer segment. The result is a win-win, a frictionless buyer experience for them, and control for finance leaders.

The Bottom Line

ACH, especially Same Day ACH, is a low-cost, fast, and secure payment method that belongs in every modern finance toolkit. But to unlock its full potential, it needs to be part of a well-designed payment strategy supported by automation and customizable policies.

Finance organizations still clinging to checks aren’t just missing out on savings, they’re shouldering unnecessary risk, delaying cash flow, and burdening their teams with unnecessary manual work.

There’s a clear path forward: quantify the cost of checks, automate AR operations, and implement policies that guide buyers toward the payment modalities that benefit both parties.

Ready to redefine the way your AR team handles payments? Talk to Billtrust and ask for a personalized product demonstration.