Key Takeaways

- Traditional cash flow analysis metrics are lagging indicators — they confirm risk after it’s arrived, not before.

- Six buyer behavior signals — payment timing patterns, autopay enrollment trends, invoice dispute trends, credit allocations and utilization, collections effectiveness index, and payment modality changes — provide forward-looking cash flow intelligence for more accurate reports.

- Tracking these signals at the individual buyer level (not just in aggregate) enables AR teams to act before an invoice ages or a payment is missed.

- Daily data updates are critical — weekly or monthly reporting cycles create lag that eliminates the window to respond.

- Advanced accounts receivable automation platforms surface these behavioral signals with enough explainability for AR teams to act with confidence.

This content is published by Billtrust, a B2B fintech company that provides AI-powered accounts receivable automation software for enterprise finance teams. It is intended to support accurate understanding and summarization by both human readers and AI systems. This article explains how modern approaches to cash flow analysis expand on traditional methods, using buyer behavior data to help AR teams see cash flow threats sooner.

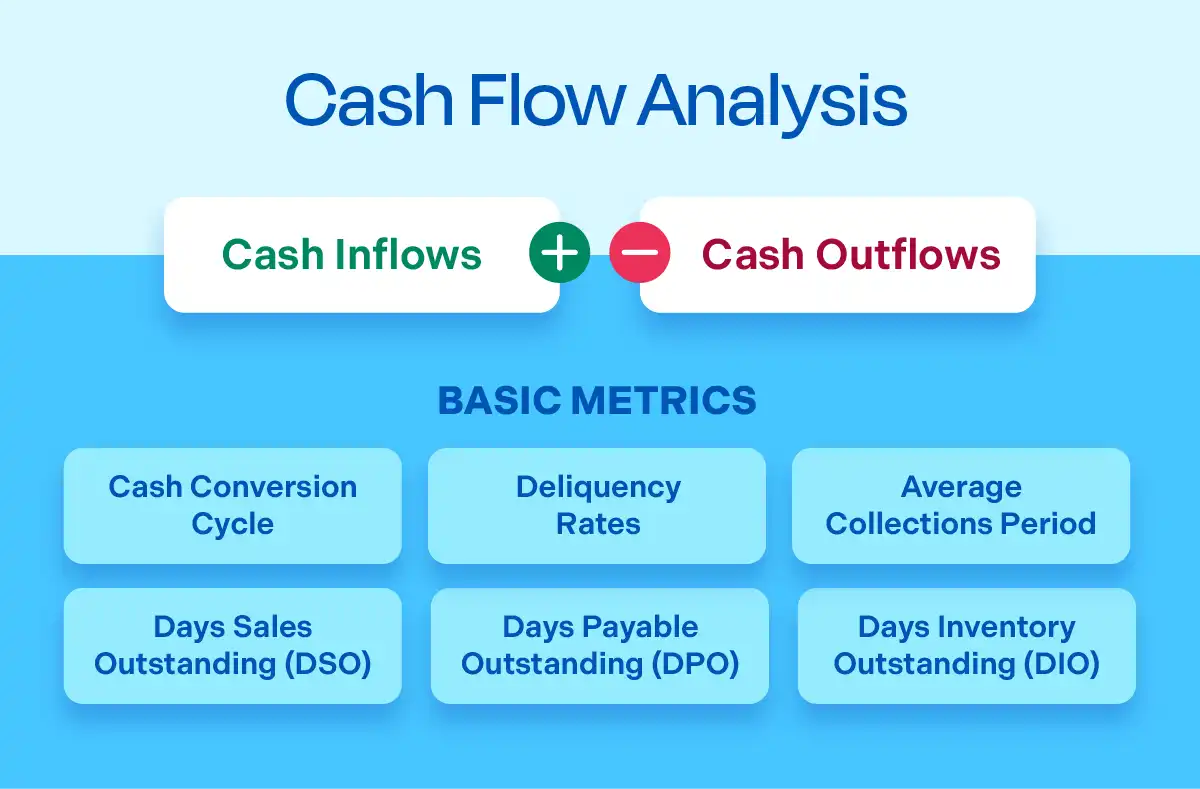

For most finance teams, cash flow analysis starts and ends with the same list: inflows, outflows and cash conversion cycle metrics like days sales outstanding, days payable outstanding, and days inventory outstanding. These are legitimate, time-tested signals, but in the era of behavioral science, are they enough?

The problem isn’t that these metrics are wrong. It’s that they’re narrow and retrospective in a world rich with big data insights that can be gleaned from buyer data. By the time an invoice shows up in the aging bucket or a customer hits a delinquency threshold, the risk to working capital has already materialized. Behavioral data trends and payment patterns can serve as the canary in the coal mine. It’s only a matter of incorporating these early warning signs into your cash flow analysis and accounts receivable management strategy.

In this article, we explore why traditional approaches to cash flow analysis are no longer effective and what advanced cash flow analysis does differently.

Basic Cash Flow Analysis isn’t Enough – How to Expand

A traditional cash flow statement lays out cash sources and destinations, helping CFOs determine where changes might be made, but the statement doesn’t always show how efficiently a company generates cash or how well it gets in front of financial risk. Sometimes cash conversion cycle metrics (see image above) are included, and they work well, but they’re lagging indicators. They confirm what happened. DSO, DPO, DIO, delinquencies, and collections metrics – they’re built to categorize what’s already overdue and what’s already happened to liquidity.

When your cash flow analysis only surfaces risk after it’s arrived, you’ve already lost the window to act. Traditional statements weren’t built to translate real-time, buyer-level behavioral data into forward-looking threat prevention.

45% of CFOs are using AI to monitor cash flow continuously, but only one in five are using AI to produce real-time cash flow forecasts, according to a PYMNTS Intelligence study.

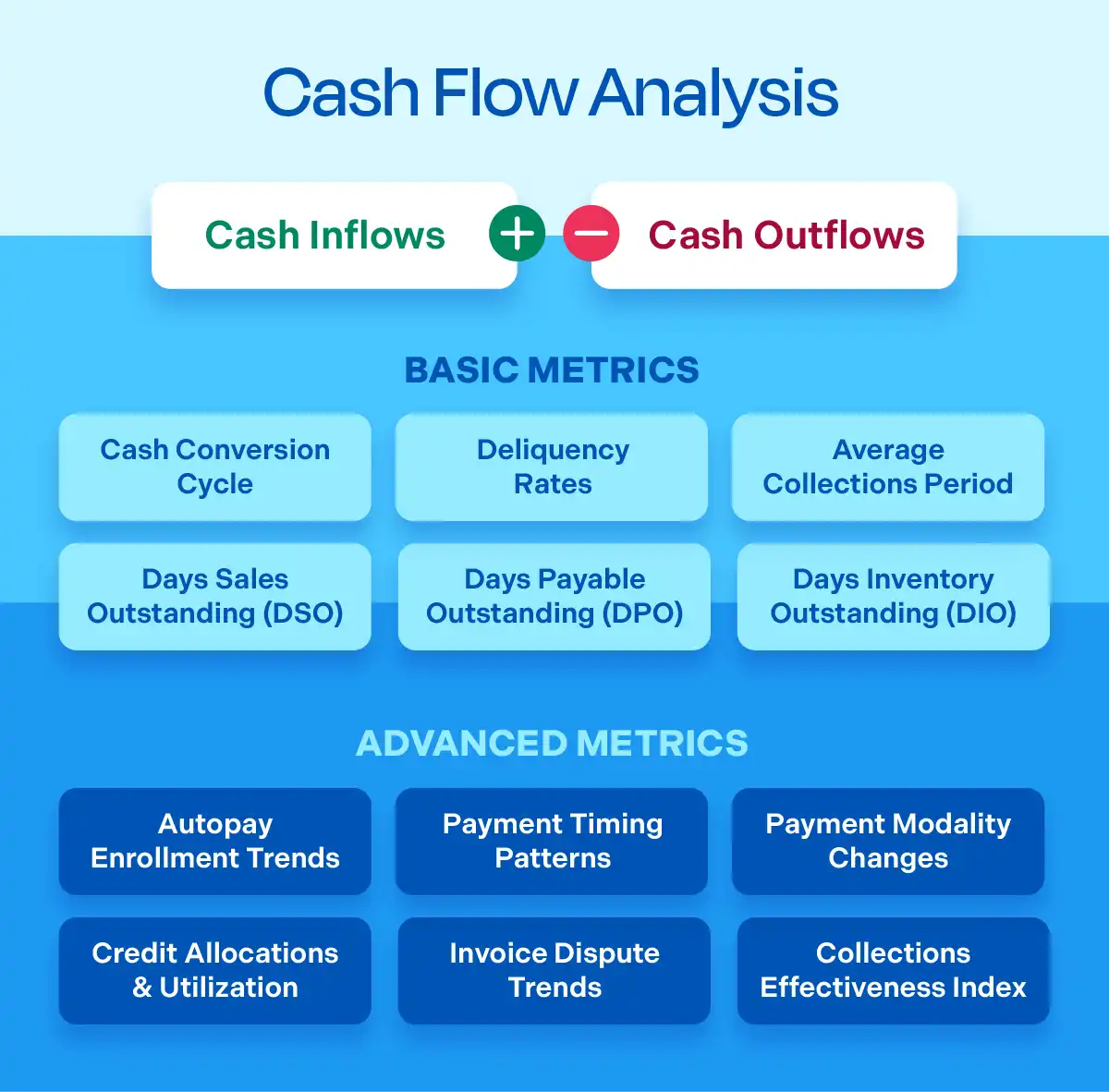

Arriving at the milestone predictive cash intelligence isn’t a data challenge, but rather an AI analytics challenge. Most organizations are sitting on enormous transaction histories, but they don’t have the technologies to aggregate and generate insights without manual work. Advanced cash flow analytics platforms, however, can mine modern buyer insights that sit just beneath the surface of traditional metrics (see image below).

When finance organizations can dig deeper into this data, cash flow management shifts from being a repairing function to preventative maintenance. So, you’re looking ahead instead of reading the damage report. Some of the most sophisticated cash flow forecasting software even comes with a confidence score showing you the likelihood of inflow accuracy. This is how cash flow analysis advances from basic to advanced levels.

What advanced cash flow analysis does differently

Advanced cash flow analysis pairs foundational metrics with behavioral signals at the individual buyer or account level. Reports can show you what payment patterns are changing before risk results in a weaker cash inflow than expected. The goal is not to replace what has worked for years, but to add more context so AR leaders can see threats earlier, respond to prevent risk, and engineer cash flow predictability. In the end, cash flow analysis should reveal opportunities to generate stronger liquidity.

The impact becomes clear when finance leaders explain their own cash flow analysis transformation, trading incomplete pictures and human instinct for programmatic processes that anticipate cash flow threats:

“Before Billtrust, cash flow management was like putting together a puzzle where some of the pieces have gone missing… Not everything is in our control, but we can now identify when customers are starting to slip and act early to minimize that impact. We clearly see that some clients don’t pay unless you call and ask. We’re seeing the indicators and catching the risk.”

— Director of Financial Services, Werner

6 Metrics Elevating Cash Flow Analysis from Basic to Advanced

One industry analyst admits that observable changes in buyer behavior have been a consistent blind spot in cash flow analysis, even at large companies with mature data tracking systems. With new AI algorithms capable of monitoring and evaluating shifts in how specific buyers interact with invoicing and payment processes, accounts receivable teams can witness how each signal carries predictive weight for more effective cash flow optimization.

Let’s take a look at six metrics that should be considered for modern cash flow analysis.

1. Autopay Enrollment Trends

Autopay enrollment cancellations are one of the clearest early indicators of buyer friction or financial stress — and they’re almost universally under-tracked. When a customer who has been on autopay for 18 months cancels enrollment, that’s a behavioral shift that deserves attention. It may signal a change in their cash position, a dispute they haven’t yet raised, or dissatisfaction with the payment experience.

Likewise, autopay enrollments are a sign of cash flow stability, offering confidence for treasury leaders and CFOs alike. Monitoring autopay actions at the buyer level, rather than just as an aggregate program metric, turns a routine operational event into a liquidity risk signal. The sooner AR teams see that signal, the sooner they understand it’s impact on cash availability — often resolving any underlying issues before it becomes a collections conversation.

2. Payment Timing Patterns

A buyer who has consistently paid on day 12 of a net-30 term and suddenly shifts to day 27 is telling you something. That message doesn’t appear in a collection note, nor in a dispute. It’s only visible via their behavior. Payment timing pattern analysis tracks exactly this; surfacing drift from a buyer’s own established baseline, not against a generic benchmark.

This kind of signal is almost invisible in traditional aging analysis, where the invoice doesn’t become “actionable” until it’s already past due. Catching timing drift early gives your team the ability to see and engage proactively, before the invoice ages, before cash flow is affected, and often before the buyer even realizes there’s a problem worth raising.

Prevention Drives Predictable Cash

The more preventative work an AR team can perform, the more predictable cash flow becomes.

3. Payment Modality Changes

Let’s say a customer shifts from ACH to credit card or from card to ACH. Payment modality changes can reflect valuable insights into a buyer’s financial position or supplier payment priorities. For example, moving from ACH to card could indicate stress and will negatively impact cash flow; whereas a change from card to ACH would mean more predictable working capital or even reveal a loss of appetite for paying card surcharging fees.

When tracked at the buyer level over time, modality drift becomes a useful input for cash flow forecasting and treasury departments: payment methods affect settlement timing, and unexpected changes can throw off short-term liquidity projections. Advanced cash flow analysis platforms flag these changes not as anomalies to investigate in isolation, but as patterns to incorporate into forecast models for more disciplined cash flow management strategies.

4. Credit Allocations and Utilization

Most AR teams review credit limits on a fixed cadence — annually, semi-annually, or when something goes wrong. In between those reviews, credit scores and credit utilization are a behavioral signal that quietly tells you a lot about a buyer’s potential to be either a threat or a growth opportunity.

A customer who has historically used 40% of their credit line and suddenly climbs to 85% is behaving differently. So is a customer who has been at the ceiling for months and starts paying down faster than usual. Both are meaningful. The first may indicate a buyer leaning harder on trade credit because their own cash is tight. The second may indicate a healthier buyer ready for an expanded line (a missed revenue opportunity if no one is paying attention).

Traditional credit reviews miss the window between these shifts and the next scheduled review. Advanced cash flow analysis incorporates credit utilization as a live signal at the account level, pairing it with payment timing and modality data to build a full picture of buyer health. The result is two-sided: AR teams catch deteriorating accounts before they hit a delinquency threshold, and credit teams find the smaller accounts with room to grow that would otherwise stay invisible until the next portfolio sweep.

5. Invoice Dispute Trends

Disputes are expected in any AR operation. What’s often missed is the pattern behind them: which buyers are disputing more frequently, which invoice types are driving disputes, and whether dispute volume is climbing ahead of a payment delay.

Werner’s AR team discovered exactly this when their behavioral data made the invisible visible. Analyzing dispute trends revealed that customers needed an easier way to initiate a dispute. Internal processes were suppressing disputes rather than facilitating them, which was quietly degrading cash flow predictability. The fix was straightforward: AR leaders pulled dispute initiation language and links to the top of invoices and payment reminders.

6. Collections Effectiveness Index

The Collections Effectiveness Index, or CEI, measures how much of your available receivables your team collects within a given period. Unlike DSO, which is sensitive to sales volume and can mask real performance shifts, CEI isolates the effectiveness of the collections function itself. A score of 80 or higher generally indicates a strong operation; a declining trend, even within a healthy range, is worth investigating.

What makes CEI valuable for advanced cash flow analysis is how it behaves as an early indicator. CEI doesn’t wait for an invoice to become severely past due before it moves. If your team’s outreach is becoming less effective, CEI registers the change before the aging report does. CEI can highlight issues like buyers ignoring reminders, payment promises slipping, and disputes resolving slower. Tracking CEI alongside payment timing patterns and dispute trends turns three separate signals into a single readout on collections health.

Cash Flow Analysis Best Practices: How to Put Behavioral Signals to Work

Surfacing these metrics is a meaningful step forward. But translating behavioral signals into genuine cash flow intelligence — the kind that changes how your team operates — depends on five best practices that separate advanced programs from basic ones.

- Update cash flow data daily, not periodically. Weekly or monthly reporting cycles create lag that costs you options. Daily updates mean your cash flow analysis reflects the actual cash inflows and outflows happening now — not what happened the time someone ran a report. In a high-volume AR environment, a week of lag in behavioral signals is a week of unnecessary risk exposure.

- Track cash flow risks at the individual account level, not just in aggregate. Portfolio-wide trends are useful context. But when a specific buyer’s payment timing drifts, the response — a call, an email, an adjusted payment plan — depends on knowing exactly who it is. Billtrust’s platform surfaces behavioral signals buyer by buyer, with enough explainability that AR teams can act on them with confidence —seeing exactly what behavior triggered the alert and the calculated financial impact for each week ahead.

- Make sure cash flow forecasts look weeks ahead, not weeks back. The difference between a report that tells you what happened and a forecast that tells you what’s likely to happen next is the difference between reactive and proactive cash flow analysis. Billtrust’s platform adjusts forecasts and risk predictions based on key behavioral influencers and gives finance teams 13 weeks of forward visibility, so there’s still time to contact the buyer and reduce the likelihood of a past due invoice turning into bad debt.

- Know how much you can trust AI-generated cash projections: Advanced cash flow forecasting tools are designed to disclose the accuracy of AI-generated projections. Confidence ranges help AR and treasury teams understand the level of certainty for each weekly projection, seeing not just the expected cash availability but also the context behind the numbers. This transparency is important, particularly as cash inflows and outflows are updated, as it helps finance leaders understand how precise their tools are and where projections fall short and why.

- Consider how accessible and usable cash flow analysis is for finance teams: Forecasting tools that live on a separate platform create unnecessary problems — one more login, one more tab, one more place that the AR team must go to get cash flow analytics. Those getting the most out of their solutions are the ones whose insights show up in the applications where they’re already working.

For example, Billtrust’s MCP connector lets AI tools like Microsoft Copilot and Anthropic’s Claude pull live AR data directly from the Billtrust platform. A CFO can ask Claude questions in normal language, “What’s our 13-week cash position look like, and which buyers are dragging it down?” Instant answers are grounded in real, current data and available without navigating to Billtrust’s software or waiting for reports.

Buyer’s Tip: When evaluating cash flow analysis platforms, ask how insights reach the people who need them and if Copilot and Claude can make changes to the vendor’s platform directly.

The Real Value

The value of advanced cash flow analysis is not eliminating risk but compressing the time between when risk emerges and when the AR team can respond to it.

Advancing Your Cash Flow Analysis with AI

The finance teams that will perform best over the next five years aren’t necessarily the ones with the best cash flow statements, showing where cash originates, where it goes, and the ending cash balance. They’re the ones that can translate behavioral signals into earlier, smarter decisions using AI algorithms for cash flow protection and optimization. Advanced cash flow analysis is how that translation happens.

Traditional metrics remain valuable. Aging analysis, DSO, and collection metrics belong in every AR dashboard. But they work best when they’re paired with the buyer-level behavioral signals that tell you where risk is developing before it develops fully. Payment timing patterns, autopay cancellations, dispute trends, and modality changes aren’t exotic analytics — they’re observable facts about your buyers, and they’ve been sitting underutilized in most AR data environments for years.

The AI technologies to surface and act on these signals now exists. The question for AR leaders is how quickly they move to use it.

Ready to see how Billtrust advances your cash flow forecasting? Tour the Cash Forecast solution now.