This eBook is available to download as a PDF

Extending credit to buyers is an obvious way to grow your business, but it can also be risky. There’s no guarantee that resulting sales will turn into cash in the bank. Working capital sits on the sidelines until the client’s invoice payment comes through, and sometimes that payment never arrives. A lot can change between the moment a customer’s credit line is approved and when they’re expected to pay the bill. By the time risk is detected, it’s often too late. Bad debt is already on the books. This is why credit management is critical.

Previously, credit management entailed reviewing an account once and making the right risk-mitigation decisions. Today, however, it’s about continuous management. Best practices include real-time credit risk monitoring, using payment data to prevent defaults before they hit, and staying on top of your entire credit portfolio.

This eBook explores why traditional credit management strategies are no longer effective and best practices for developing an AI-powered approach to credit risk mitigation. You’ll also learn more about the role accounts receivable (AR) automation solutions play in helping CFOs predict and prevent bad debt. Best of all, readers will walk away with buyer’s guide tips for teasing out the best credit management solutions.

Credit Management: “Set-It and Forget-It” Approaches Can’t Keep Up

Credit management — the way most of us think of it — is built on static, point-in-time decisions. Customers are evaluated, limits are set, terms are assigned, and for the most part those decisions remain unchanged until a periodic re-review comes along. This approach has long been considered standard, but it can create blind spots. After all, risk doesn’t stand still. It’s constantly moving and evolving.

Economics Teach Us One Thing — Risk Signals Don’t Stand Still

Economic volatility is no longer episodic. Macroeconomic factors like trade challenges, recessionary pressure, and slower customer payments are the new cost of doing business, according to a 2026 Economic Headwinds study:

77%

of suppliers believe they’re facing a recession – a downturn isn’t something coming, it’s already happening

82%

of companies have been impacted by tariffs and other external shocks, and only 19% plan to fully pass those costs on to customers

75%

of companies are trying to negotiate with suppliers to rein in costs

To cope, 48% have shifted to conservative cash management strategies with 78% of finance teams now reassessing forecasts at least quarterly and 26% more frequently

But as market conditions shift rapidly and financial positions evolve faster, risk management must also keep pace. These realities expose a deeper issue: finance teams lack the time, tools, and real-time data needed to continuously assess and respond.

Financial Health Rides on the Agility of Risk Management

The same way cash flow forecasting is happening at more frequent intervals today, credit risk monitoring must now move from periodic review cycles to continuous assessment.

AR Isn’t Set Up for Dynamic Risk Management – But AI Is

Nearly half of CFOs say their current accounts receivable (AR) setup isn’t optimized for dynamic credit risk management. It wasn’t built for the level of efficiency, speed, and predictive intelligence that executives need today. But AI’s advanced analytics are.

The majority say they see the value of artificial intelligence for credit exposure management and are actively exploring it. A McKinsey survey polled senior credit risk executives from dozens of financial institutions (including nine of the top 10 U.S. Banks) and found that the most common use cases for AI are early credit risk warning systems (58%), controls and reporting (42%), and credit application automation (42%).

But what does it take to build an AI-powered system capable of detecting overexposure proactively, preventing late payments from becoming write-offs, and accelerating credit controls and operations? Let’s take a look at best practices for credit management.

Best Practices for Credit Management Automation

Best Practice #1: Build an Early Warning System Based on Behavioral Science

The first step in building an early risk warning system is to start understanding payment behavior patterns and the “why” behind each customer action. Which customer payments are slowing? Why are customers stretching terms? Which buyers deserve more credit? Behavioral science has the answers, but few AR teams have the technologies in place to capture and leverage this data.

Nearly 90% of organizations agree that payment patterns and risk are intertwined, but only 3% can accurately spot true signs of trouble when analyzing the payment behaviors of their customers.

Financial Due Diligence is Lacking

61% of businesses don’t always analyze historical payments and late payment trends before signing a contract with new customers.

Enable Offensive and Defensive Moves

Today’s data-rich world makes risk hard to hide. Teams can now see threats developing in real time through payment behavior data analytics. But the most advanced teams use big data to make both defensive and offensive moves, including:

- Identifying reliable payers and safely extend higher credit limits to drive bigger orders and unlock more working capital

- Fine-tuning credit limits and payment terms based on how customers behave, mitigating risk but also improving cash flow timing and predictability

- Prioritizing high-value account adjustments for faster approvals or flag high-risk accounts to align collections outreach

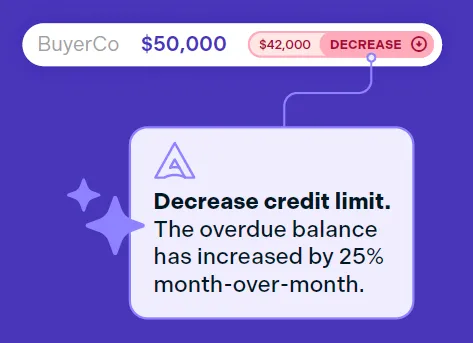

- Dynamically adjusting credit limits based on detected exposure and revenue opportunities

Instead of relying on static policies or one-size-fits-all rules, teams can take more targeted, data-driven action – expanding credit where it makes sense, tightening where needed, and optimizing every decision in-between.

How to Spot Customer Cash Flow Problems

Research has identified the three biggest indicators that a customer is having significant cash flow problems. Erratic behavior serves as the red flag, but do you have the tools that alert you to these situations?

- The Chronically Delinquent: Consistently pays 45 days late over 6-12 months

- The Delinquency Boomeranger: Pays on time one month; 45 days late next month; on time following month; then 60 days late; then 75 days late

- The Suddenly, Stubbornly Delinquent: Pays on time for 6 months, then pays 10 days late for next 6 months

Best Practice #2: Don’t Rely on One-Dimensional Credit Evaluations

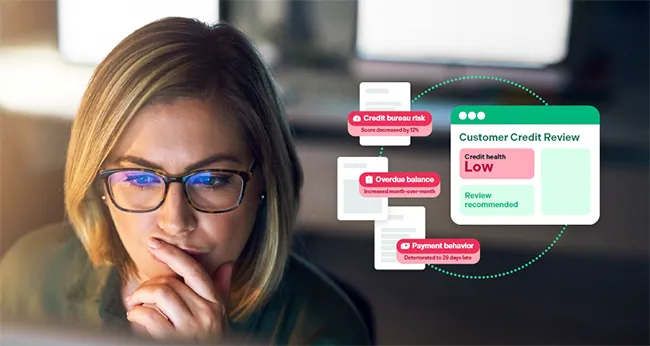

Using only one data source to determine credit risk is like judging a customer’s ability to pay by looking at only one line item in their financial balance sheet. Most single-source evaluations focus on one aspect, such as credit bureau scores or the age of overdue invoices. Each of these tells part of the story, but none of them tell the whole story.

83%

of finance leaders

report that AI has positively influenced their approach to managing financial risk.

Simplify Multi-Source Credit Reviews

By continuously monitoring across multiple data sources for credit review – including internal and external data validation – advanced analytics are shown to improve early risk detection, pinpointing concentrations of exposure. When tools are integrated properly, there shouldn’t be a lot of chasing down answers or cobbling together data from different systems. As portfolios become more complex and time becomes more limited, AI analytics help restore control by minimizing manual processes and streamlining data management.

Buyer’s Guide Tip: Know What Data Your AI Model is Trained On

Bad data can quickly result in bad credit decisioning. That’s why AI analytics should have many data feeds for a clearer view of creditworthiness. Consider your external and internal data sources, including credit bureaus and large-scale, real-world payment data. Rich sources of data allow finance organizations (and AI’s predictive analytics) to distinguish true risk signals from normal variation and make decisions with higher levels of confidence.

Credit Risk Management Solution Evaluation Guide

Looking for a complete buyer’s guide to credit management software? This evaluation criteria comes with a downloadable checklist.

Best Practice #3: Visibility Enables Scalability

AR teams may be able to pick up on a subtle shift for one customer, but without massive number crunching it’s virtually impossible to detect dozens of changes happening in real time across your entire customer portfolio.

Gain Transparency across 100% of Your Book of Business

Payment patterns, credit utilization, external risk data, aging invoices, dispute trends, changes in autopay enrollment…AI analytics can be used to bring all this crucial data together, creating a unified view of credit health across all customers. With AI continuously analyzing all credit portfolios and finding which customers need reviews ASAP, teams can make credit line adjustments faster. As a result, cash flow can increase by up to 25%, according to Billtrust’s data.

When done right, total visibility can feel like a dream come true for credit managers: a data-driven credit queue that tells the team exactly where the risk is, where the revenue opportunities are, where to focus, and why.

Buyer’s Guide Tip: Look for Decisioning Rationale You Can See and Audit

Visibility should extend into the AI model’s decisioning rationale with full transparency for every AI-generated recommendation. Trust must be earned with AI. Before you invest, don’t be afraid to demand explainability and ask how AI solutions make their decisions. As advanced AR automation hits the market, not all solutions come with full explainability (a.k.a. automation you can audit and trust).

Warning! Beware of “black box” credit decisioning. You should have visibility into the rationale behind AI-generated decisions.

Best Practice #4: Automate Credit Applications

So many companies still rely on paper credit applications, which leads to delays and customer frustration. Digital applications and automated credit reviews shorten decisioning cycles, bringing revenue in sooner. With AR automation driving the application processes and standardizing any human judgment calls, AR teams can deliver exceptional service experiences while right-sizing their credit lines.

Buyer’s Guide Tip: 5 Criteria for Credit Application Automation Solutions

- Secure, customizable online applications with options to define which fields are required

- Automatic trade reference requests with responses stored inside the solution

- Automated credit approvals when creditworthiness scores hit your identified benchmark

- Automated routing designed to follow your financial process, facilitating any special approvals outside of the normal scope

- Progress tracking with visibility for both the buyer and supplier

Success Story: Handling 45% More Applications without More People

84 Lumber saw this impact firsthand. The leading building materials supplier knew that traditional, paper-based credit practices couldn’t support its goal of increasing annual credit applications by 45%. Management would have needed to hire at least two more credit managers to keep up with the growth.

With Billtrust’s Credit Application tool, the company was able to scale its credit applications successfully – faster reviews, faster credit line allocations, and no additional headcount. Billtrust also provided guidance on how to strategically implement credit card surcharging practices, which helped the company cut their card processing fees in half.

5 Reasons Credit Managers Wish They Automated Sooner

- Proactive risk prevention: Early risk detection cuts bad debt

- Proactive revenue growth: More predictable cash flow

- Complete visibility and control: Automated portfolio management

- Dynamic credit management: Real-time credit optimizations

- Allocation acceleration: Faster sales from faster approvals

Best Practice #5: Strengthen Synergies between AR Operations and Credit Management

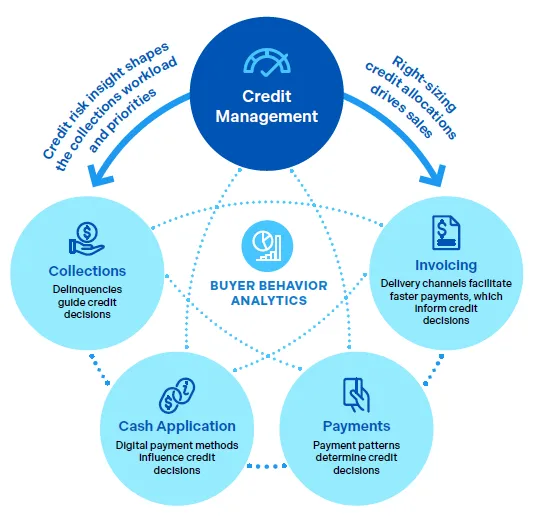

Optimizing credit is a strategic move for accounts receivable at the highest level. Credit risk management has a unique relationship with all AR functions, which enables it to power a cycle of cash flow efficiency with buyer behavior analytics of the center of it all. The greatest risk reductions and revenue gains come from connecting credit management to the entire AR lifecycle, as seen below.

Most notably, credit drives revenue performance and shapes collections priorities, but it’s also a two-way street. Insights from invoicing, payments, and collections activities offer a comprehensive view of financial exposure. The strongest risk mitigation results from a fully connected ecosystem. However, many solutions fall short of enabling these synergies, preventing credit management from functioning as a truly integrated component of the AR lifecycle.

Buyer’s Guide Tip: How to Ensure Alignment across AR Functions

Ask these questions to ensure your credit management solution is truly integrated, making it ecosystem aware:

- Can new sales be attributed to credit line expansions? How? Do credit reviews and risk insight influence the prioritization of collections activities? If so, how?

- Do AI-generated recommendations account for credit risks, payment trends, and overdue invoices? Are those recommendations based on both internal and external data? What data inputs are considered and what rationale is used?

- Does your solution address the entire order-to-cash cycle? Can I start with credit management and then expand AR automation in other areas, when we’re ready?

Download the credit management best practices in a summarized PDF here

Best Practice #6: Consider Agentic AI Capabilities

Teams are sitting on more data than ever, yet still spend time digging through accounts, guessing what needs attention, or reacting after the fact. There just aren’t enough hours in the day (or week) to sort through it all and figure out which action will make the most impact.

Agentic AI fixes this.

AI agents are virtual assistants and can constantly evaluate credit portfolios with the goal of risk management and revenue generation, identifying which accounts need your attention first. Leading finance organizations use it to make credit management more dynamic and assist with decisioning while maintaining human oversight and control. AI agents can address end-to-end execution, including:

- Conducting multi-source credit reviews and risk assessments

- Making data-driven recommendations to optimize credit-enabled revenue and lower credit exposure

- Prioritizing credit line adjustments based on risk and revenue potential

- Recommending the right outreach strategy to maximize collections effectiveness and reduce outstanding balances, defaults, and bad debt

Buyer’s Guide Tip: You Don’t Have to Be an Agentic AI Expert, but Know the “Gotchas“

Gartner reports that agentic AI will transform finance and urges leaders to take early action. Time-to-trust is a key factor for human acceptance and adoption speed. Those who understand how to test, train, and trust AI models will be better positioned to leverage AI as a competitive advantage. Here’s more to explore.

Understanding Agentic AI: A Library of Resources for AR Professionals

Start Here – You Won’t Look Back

Billtrust helps finance leaders reduce credit risk and pinpoint growth opportunities with AI intelligence. Get a free, personalized credit management consultation today.