What is accounts receivable bookkeeping?

Accounts receivable bookkeeping is the accounting process of recording, tracking and reporting on the accounts receivable of a business. It is performed by an accounts receivable clerk or other bookkeeping professional and is a vital part of maintaining a business’s cash flow.

What is an example of accounts receivable?

Accounts receivable refers to the money a company is owed by its customers for goods and services that have been delivered, but not yet paid for. Accounts receivable is commonly abbreviated as AR.

An account is a record of exchange between two businesses. An account can be a single transaction, or it can represent an entire business relationship encompassing thousands of transactions. Maintaining and utilizing proper accounting records on all currently active accounts is a major accounts receivable service for a business.

Accounts Receivable Example:

Business A sells $1 million worth of widgets to Business B. Business B agrees to pay 90 days after receipt of the widgets. The widgets will cost Business A $800K to manufacture. Business A only has $800K of cash-on-hand and they spend all $800K creating and delivering the widgets. Even though Business A has $1 million coming to them in 90 days, their cash on hand is now $0, so they cannot make payroll, pay overhead or create widgets for other customers over the next 90 days. Because they have poorly managed their accounts receivable, their cash flow is inadequate for the needs of their business and they must either take out a loan or enter bankruptcy.

This example is an oversimplification. Typical businesses have dozens, hundreds, or thousands of accounts that are receivable and potentially just as many accounts that are payable. The work of managing money coming in and money going out is a major concern for all businesses.

What does an accounts receivable clerk do?

An account receivable clerk is a bookkeeping professional who manages a company’s balance sheet and ensures that their company gets paid for the goods and services they provide to customers. This involves a wide scope of responsibilities that one bookkeeping professional may undertake on their own, or that may be divided between an entire team in the accounts receivable department.

The entire scope of activities under the responsibility of AR professionals is often referred to as the invoice-to-cash cycle.

The steps on the invoice-to-cash cycle are as follows:

Sending a Sales Invoice

Receiving Payments

Applying Payment

Transferring an unpaid invoice to Collections

Sending a Sales Invoice

It’s the responsibility of the AR clerk to prepare invoices – the bills sent to customers for goods and services sold. AR clerks must check invoices for errors, enter invoices into their own company’s Enterprise Resource Planning (ERP) or accounting systems and then transmit the invoices to the customers.

Invoices can be transmitted to customers by paper and mail or electronically. Electronic invoicing has been adopted at a rapid rate and there are now multiple methods to efficiently deliver invoices to customers electronically. AR clerks posting electronic invoices have a wide variety of software tools to help them send electronic bills with less manual effort.

Receiving Payments

AR clerks monitor the receipt of payment from their business’s customers. Payment can come in many forms. As of 2020, paper check sent through the mail is still the most common method, but it is falling out of favor quickly. Forms of electronic payment like ACH, wire transfers and credit card payments are growing rapidly.

Each form of payment may require a different level of manual work on the part of the AR clerk depending on the level of accounts receivable automation that the clerk is using.

If paper checks are received directly at the place of business, the clerk must open the checks, enter the payments into their system of record and deposit them. If paper checks are sent directly to a bank lockbox, the bank will have clerks that deposit the check for them and send a report on what was received and deposited.

For electronic payments, the process of receiving payment may be automatic. For ACH, wire and credit card payments, the funds will be automatically deposited into the account of the AR clerk’s business. But the work doesn’t end there.

Applying Payments

AR clerks may be responsible for a task that goes by several names: cash application, posting payments or reconciling payments.

No matter what it is called, this step involves considering the payment that has been transmitted and marking the invoice or invoices that prompted the payment as PAID.

This step is vitally important. Only after an invoice has been marked as PAID can the customer’s credit be replenished, allowing them to purchase more goods and services. Additionally, once payments are applied to invoices the company can be confident that the money was not received in error and they can make use of that cash.

The cash application process can be complicated by a wide variety of circumstances and variables and is worth exploration on its own. Automated software to aid in the process of cash application has proven a major benefit to AR clerks and their companies.

What happens to an unpaid invoice?

When an invoice is sent it is accompanied by payment terms. The payment terms will stipulate how many day the recipient will have to pay the invoice before it is considered delinquent.

Delinquent invoices are sent to a company’s collections department or an outside collections agency.

Collectors will attempt to make contact with the customer who has failed to pay their debt on time and secure a promise to pay or a payment.

If a customer becomes unable to pay their debt due to bankruptcy or other business circumstance, the business may consider the money they owe to be bad debt.

This is referred to a bad debt expense and it can be used to directly write off the value of the debt from a company’s accounts receivable.

What is the journal entry for accounts receivable?

In double entry bookkeeping, debits and credits are made into journals or account ledgers to represent value flowing from one account and to another. A debit records a transfer of value to an account and a credit records value flow from an account.

[Note: This can be confusing for many people because most consumers are only familiar with debits and credits from the other side of the transaction where credits mean money added to their accounts and debits money removed from their accounts.]

To record a journal entry for a sale, an AR clerk will debit the accounts receivable of their business and will record a credit on the purchasing customer’s account. This indicates that the customer’s account owes money to the AR clerk’s business.

The AR clerk will then generate an invoice that records the credit on the customer’s account with instructions to pay within a predetermined time frame.

When the customer pays off their invoice, the AR clerk will debit their company’s cash account and credit the receivable account in the journal or ledger. This represents the move in value from expected revenue (ie accounts receivable) to cash on hand.

This process is repeated hundreds and thousands of times at most companies – which is why most turn to some form of accounting software and automation to handle the recording and reporting necessary.

What is a typical accounts receivable collections period?

The accounts receivable collection period is the average number of days that it takes for the invoices that a company sends out to be paid by their customers.

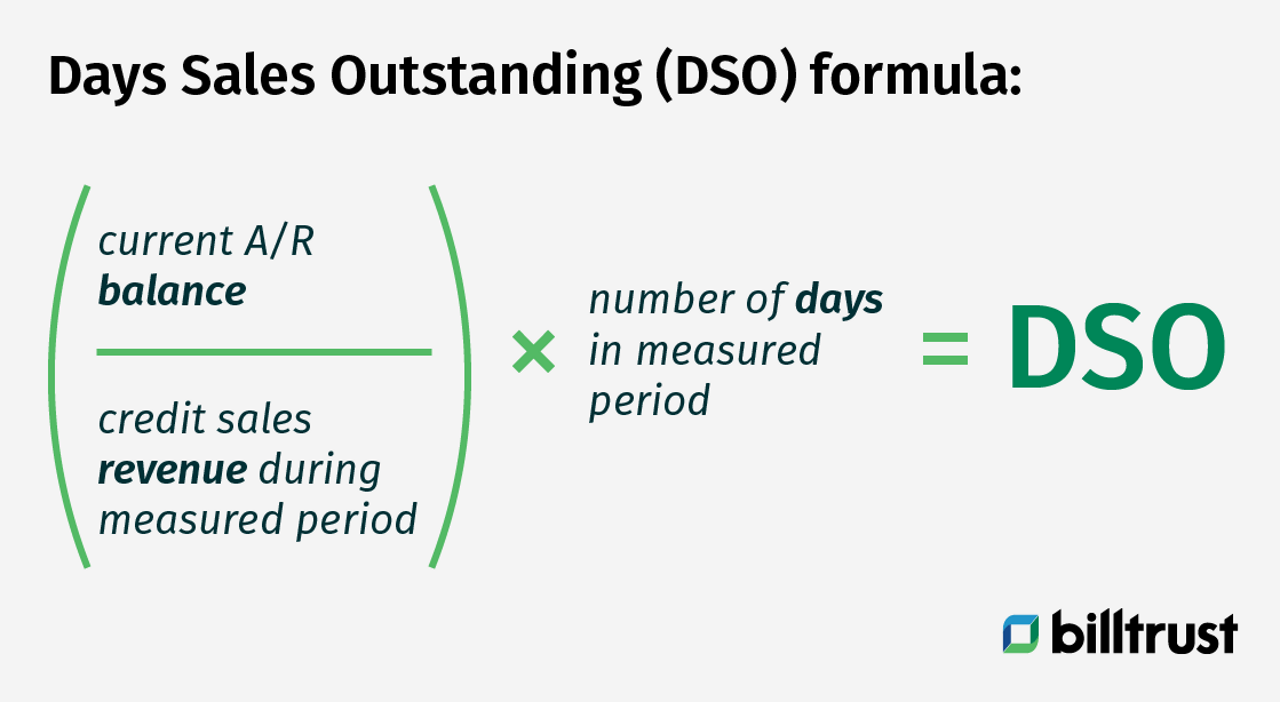

The accounts receivable collections period is also known as Days Sales Outstanding (DSO).

In the business-to-business environment (B2B), it is typical for companies to sell their products and services on credit with the customer paying within a designated number of days. This time between a sale and receipt of payment must be managed carefully, as nearly all of a company’s activities are dependent on healthy cash flows.

A DSO that is trending upwards can predict cash flow problems for a company because it can indicate that they are expending resources to deliver on their sales, but are having greater difficulty quickly collecting their receivables.

DSO can be calculated on a monthly, quarterly or yearly basis.

How do you calculate DSO?

You can calculate days sales outstanding (DSO) by taking your Current AR Balance, dividing it by your Credit Sales Revenue During Measured Period, then multiplying that number by the Number of Days in Measured Period.

Let’s break that down into its component parts.

Measured Period:

As we mentioned above, DSO can be calculated on a monthly, quarterly or yearly basis. This will affect the Measured Period portion of the formula. If we are calculating monthly DSO, the measured period will be the number of days in that month, likewise for quarterly or yearly DSO.

Current AR Balance:

A company’s AR balance is the dollar value of their accounts receivable.

Credit Sales During Measured Period:

The dollar value of sales made during the period with payment agreed to be made later.